There’s No Time Like the Present to Make a Plan for Your Loved Ones’ Future

TL/DR: The answer to when you should start estate planning is now, even if it’s just making a plan to make your plan. You do not have to have every detail figured out before you start; pausing and reflecting are expected parts of the process. Just be prepared to put some thought behind questions you’ve never had to think about before about your relationships, your legacy, and your values. The reasons for having an estate plan differs for everyone, but what doesn’t differ is the benefits that come from making a plan sooner rather than later.

This article dives further into the specifics of when you should start estate planning.

Are you someone who panic-cleans before guests come over or only flosses the few weeks before a dentist appointment? Sometimes trigger events like these can provide an incentive for us to kick good habits into gear.

Many people similarly put off estate planning until they experience a trigger event, such as a death in the family, the birth of a child, or experiencing the pain of probate when a family member passes away.

Writing a Will or completing the other important steps in estate planning isn’t at the top of many people’s to-do lists. The process is unfamiliar, seemingly complicated and expensive, and, let’s face it, forces you to think about your own demise. Not a fun weekend activity. We get it.

But there’s no time like the present to prepare for what will ultimately be the future.

“If you wait to create an estate plan and the unexpected happens, you’ll be leaving your loved ones in the lurch,” says Anne Rhodes, head of legal at Wealth.

“You have the luxury of time right now to be thoughtful about what you would want to happen to your financial affairs and your health care, and to discuss these topics with your loved ones. By the time your loved ones are being asked by a judge or a doctor what you would have wanted done, it is too late. Plus, your loved ones are probably upset and tensions may be running high. Having an estate plan minimizes the confusion, anxiety, and agony that can result from making the types of decisions about assets and medical treatments that sometimes tear families apart.”

When Should I Make a Plan?

If you’re reading this and you don’t have an estate plan, the answer is: Now. As soon as you become a legal adult at age 18 (and in some states, even younger!), you are able to make an estate plan. Once you start owning things – a savings or investment account, 401(k), life insurance, or real estate – you need to make decisions about who will receive those things when you die. Equally important, you need a health care power of attorney and a financial power of attorney in place so someone can make decisions on your behalf if you become incapacitated.

Once you reach other milestones—moving to a different state, getting married or divorced, having kids, retiring—you’ll need to update your estate plan to reflect those changes.

Why Should I Make a Plan Now?

An estate plan is about so much more than deciding who gets your stuff. “It’s about giving peace of mind and certainty to your loved ones on questions that might become contentious or agonizing for them, including who gets to speak for you, who gets to pick through your jewelry box, and withdrawing life support,” Rhodes says.

Think broadly of what encompasses an estate plan. This includes not only signing a Will and an advance health care directive, but also leaving your executor with a roadmap to find and access your assets; getting life insurance if you are the primary breadwinner and you have dependents; and writing down your wishes on end-of-life support and organ donation. Without an estate plan, you are leaving your loved ones to fend for themselves and to make the difficult decisions while guessing at what you might have wanted for yourself.

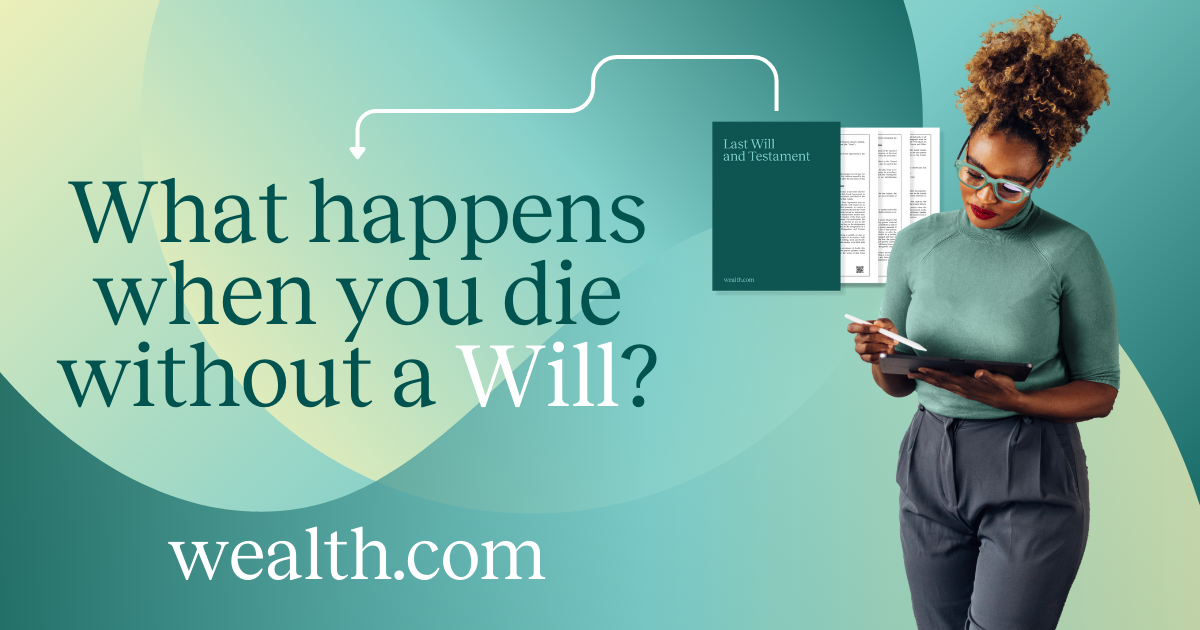

Without a will or trust, even simple estates will probably need to go through probate, delaying the dispersing of your money and property and potentially splitting up your estate in a way you wouldn’t have wanted.

If your family situation is more complicated—you have a significant other you’re not married to, you have a blended family, or you own a business—be more complicated, more expensive, and take even longer. Your loved ones might be waiting a long time before they receive anything from your estate.

One of the other important reasons to make an estate plan, of course, is to name guardians for your children. If you and the other parent were to both be incapacitated before your child turns 18, naming a guardian in your Will is the only way to make sure you have a say in who will care for your child.

Spelling out how you want your estate dispersed also can preempt family squabbles about who gets how much.

So, what are you waiting for? You can start estate planning today by following this link.