Thank you for being part of the wealth.com community. We always want to keep you up-to-date with our latest features available. Below, please see the newest features we launched last month. If you have any feedback or questions, we’d love to hear from you: [email protected].

Will & Trust Owner’s Manual

Created by expert in-house trust and estate attorneys, this propriety resource includes information about owning a Will, managing a Trust, and guidance on how to fund or transfer assets into a Trust.

Help Center

The new digital resource center is now available in-app. From getting started to understanding more complex estate planning questions, this information simplifies the process. If you still have questions, we are here to help: [email protected].

In Case You Missed It

A few noteworthy features to check out:

Attorney Consultations: Through our preferred attorney network, vetted extensively and available in all 50 states and DC, you can now connect directly with expert trust and estate attorneys in your state without leaving the app.

Asset Aggregation & Ownership: Securely connect to over 10,000 financial institutions and take advantage of integrations with Coinbase, Carta and Zillow. Stay organized and better understand the full structure and value of your networth, including how assets are owned.

Wealth Projections: Know your future net worth, the potential impact of federal estate taxes on your taxable estate, and get a better sense of what your beneficiaries may receive.

We want to hear from you. Please share your feedback with us!

We are excited to announce that we now offer the ability for married members in common law states to draft Joint Revocable Trusts.

Wealth.com always seeks to provide meaningful solutions to our advisor partners and their clients. We have offered Joint Revocable Trusts to our members in community property states since our launch. Based on the demand for this feature in other jurisdictions, we have partnered with advisors and our legal experts to expand this feature to common law states.

For members who are unsure what type of Trust document makes sense for them, the Wealth.com platform has an embedded intelligence layer to help members select the Trust type that best suits their needs, including the member’s state of residence and marital status. For example, for married couples in community property states (AZ, CA, ID, LA, NV, NM, TX, WA, and WI), a joint revocable trust might be most appropriate to simplify the administration of their community property.

For couples living in common law states (all other states), it may be most appropriate to prepare two individual revocable trusts. Traditionally, estate planning attorneys in common law states prefer for couples to sign two individual revocable trusts for three main reasons:

1. When each spouse has their own trust, this increases the flexibility for each person to uncouple decisions regarding trustees, beneficiaries, and assets to be transferred into the trust. This can be particularly important for blended families or couples established later in life.

2. A joint trust can create confusion over asset ownership for income tax reporting and opens the possibility of inconsistent income tax filings, which the IRS may not respect upon audit.

3. The probate and trust administration process may be more efficient if only one person’s trust is involved at that person’s death. For example, if there is an issue about the validity of the document or someone sues the estate of the first spouse to die, the estate plan of the surviving spouse will not be implicated.

However, circumstances and priorities vary, and some use cases warrant the need for a joint revocable trust regardless of your state. We are pleased to now deliver this to our members.

Our platform is designed to guide members to make decisions based on their own unique needs, including the proprietary evaluation form to understand what documents are appropriate. Members that would like additional platform support or education can also speak with our success team through phone, chat, or email ([email protected]). For those that are in need of legal advice, they may choose to consult with an attorney through Wealth.com’s preferred network at any time.

Additional Information: Please note that at this time, members in Georgia and New York are not able to create Joint Revocable Trust, but this capability will be coming soon and you can always reach out to your Partner Success Manager for more information.

At Wealth.com, we are proud to deliver a seamless and worthwhile experience to our members. Our product innovation is driven by our commitment to partnering with our advisors and their clients to find solutions to their problems. For our June update, we’re excited to share new releases. We welcome any feedback or questions: [email protected]

Spotlight: Updated Advisor Dashboard featuring the Activity & Insights Feed

We released an updated design of our Advisor Dashboard. Alongside a sleeker feel, we’ve also enabled an Activity & Insights feed that provides our partners with information about their clients’ latest activities.

This feature reflects our commitment to creating transparency between advisors and their clients, facilitating effective and ongoing dialogue about financial and estate planning.

Help Center

Wealth.com was built to take the stress and complexity out of estate planning, empowering people to create plans that secure their future. We’re committed to empowering our partners and members by providing them with the answers they need, when they need them.

We’re excited to share that we now have a Help Center available in-app for both members and advisors. These tools provide answers to frequently asked questions, as well as information about estate planning.

Having a digital Help Center — in addition to educational videos and our Member Success team that offers email, phone and chat support — is part of our dedication to making sure that no matter how you prefer to access information, we have something that works for you.

Wealth.com advisors and members can check it out here.

In Case You Missed It

Members expressed needing to speak with an attorney, so we made that process easy. Through our preferred attorney network, vetted extensively and available in all 50 states and DC, members can now request to speak with expert trust and estate attorneys in their state without leaving the app.

We want to hear from you. Please share your feedback with us!

TL/DR: Estate planning isn’t as complex as it may seem and you don’t need a legal degree to create one. In short, estate planning is simply recording your wishes for what happens if you’re unable to manage your own affairs. This quick and comprehensive overview will give you a working understanding of the estate planning basics.

No one likes to think about death, especially their own. But think about this: What will happen to your stuff—money, family heirlooms, even a pet—if something happens to you? If you haven’t created a document that tells your loved ones who should get what, and who should sign off on those decisions and do all the paperwork, your loved ones will have to decide for (and potentially argue among) themselves. You can provide for your family’s needs, ensure your wishes are honored, and save your loved ones a lot of anguish during an already stressful time by creating an estate plan.

Although estate planning is essential for ensuring your money and property are distributed in exactly the way you want, only one-third of adults in the U.S. have a Will. That overall number has fallen steadily over the past five years, but the COVID-19 pandemic did inspire those ages 18 to 34 to write a Will—63% more people in that age group created a Will in 2021 than in 2020.

So why don’t more people do it? The five main reasons are:

I just haven’t gotten around to it.

I don’t have enough money saved.

I don’t know how to begin.

I don’t know anything about it.

I don’t own anything valuable.

Unfortunately, these misconceptions are preventing people from putting even a basic plan in place. People perceive estate planning to be complicated, scary, or simply not relevant to them. The reality is, you don’t have to be a millionaire or own multiple homes to benefit from an estate plan.

You need an estate plan if:

You worry that your pet(s) could be given to a shelter

You want to make a final gift to a grandchild, niece, or nephew, or a friend or charity at your death

You have specific wishes about your health care and end-of-life care

You feel strongly about who should manage your affairs if you were unable to do so yourself

You really want your children to end up with your assets, if there is anything left after your spouse passes away

Some of your family members don’t get along and might disagree about who gets what or who should manage your affairs

You do not want a certain family member to receive your assets, to make health care decisions for you, or to manage your affairs

You own a significant amount of cryptocurrency

Do any of these sound like you? Because most everyone can benefit from the peace of mind an estate plan brings, we want to demystify the process so everyone—yes, even those without a law degree—can see that it’s simpler and more accessible than they think. And, hopefully, the information in this guide will equip you with enough information to quit putting off this important task.

Getting Started: Estate Planning Documents

At its most basic level, estate planning is making preparations for when you’re no longer able to make decisions for yourself. It requires creating and signing a few legal documents; but more importantly, it requires thoughtful decisions so that the money and possessions you have earned and accumulated can be passed down to your family or whomever you choose.

Let’s talk about what you’ll put in place as part of a basic estate plan. The legal documents are:

Last Will and testament: This document, which becomes active after you die, expresses your wishes for how to divide up your property and possessions and names the people you prefer to manage your financial affairs (the “executor”) and take care for your children who are minors or have special needs (the “guardian”). A revocable Trust can offer some advantages over a Will (more on Trusts vs. Wills here). However, you can only designate an executor or a guardian through a Will, not a Trust. For this reason, you still need a short Will (called a “pourover Will”), even if the centerpiece of your estate plan is a Trust.

Financial power of attorney: Think of this document as a permission slip that gives the person you name (the “agent”) the ability to conduct financial transactions, sign documents, and make other legal decisions as if they were you. In most states, you can choose if your agent has this permission immediately after you sign or only once you are incapacitated. This document terminates at your death.

Advance health care directive: This document empowers the person you name to make decisions about your medical treatment, symptom management, and end-of-life care. Depending on your home state, this document may go by a variety of different names, including a health care power of attorney or proxy. The document usually includes or is paired with a living will, which are your written instructions for health care providers about the type of life-prolonging medical care you want to receive if you are unable to make decisions for yourself.

Trust: A Trust is created by a contract or agreement and acts like a bucket of “stuff.” The Trust agreement is the set of rules that the creator of the Trust puts in place for the trustee who oversees the Trust. The rules include what powers the trustee has over the Trust, to whom and under what circumstances the trustee can give assets out of the Trust. After you create a Trust, you can transfer your assets into the Trust right away, before you die. There are many types of Trusts that accomplish different goals. If you create a Trust as the centerpiece of your estate plan instead of a Will (more on Trusts vs. Wills here), you will set up a type of Trust called a “revocable Trust” or “living Trust.” You will be the trustee of your revocable Trust in the beginning. You can also designate the person who will step in for you as trustee so that when you are unable to manage your own affairs eventually, that successor trustee can distribute your stuff according to your instructions. Unlike a Will, a Trust is active the day it is created, which means that your successor trustee can also help you manage the stuff inside of your Trust in case you are incapacitated.

There are two types of Trusts.

Revocable or living Trusts can be altered at any time by the creator of the Trust (you). These Trusts are often used as a substitute for a Will in estate planning.

Irrevocable Trusts are difficult and expensive to alter once created. They can be used to achieve many types of goals, including minimizing taxes protecting assets from creditors, naming an adult to manage property for children before they reach a certain age, and ensuring that assets stay within the same family. In your Will or your revocable Trust, you can instruct your executor or trustee to create an irrevocable Trust to take advantage of the benefits of irrevocable Trusts.

Why Do I Need an Estate Plan?

No one needs an estate plan. That is, unless you want to avoid confusion, chaos, hurt feelings, family drama, and delayed distribution due to probate. So, maybe you do need one?

An estate plan lets you give the gift of clarity to your loved ones—and does all the legal heavy lifting so they don’t have to. When you spell out your wishes in the legal documents listed above, there’s less second-guessing about your intentions for how your stuff should be distributed.

The opposite is true if you die without a Will or Trust in place. Legally, you are dying intestate, and your home state’s succession laws will determine how your assets will be distributed and to whom. These succession laws differ from state to state, but were likely drafted a long time ago, based on the most common wishes of a typical, American nuclear family, and likely do not reflect the complexities of your family and cultural heritage.

By not creating an estate plan, you are just letting the state legislature from decades ago take a guess as to what your wishes are. This is especially true if you’re single and don’t have dependents.

You may own assets that will not pass through your estate, either because of the title on the asset or because you designated a beneficiary. For example, jointly owned property–real estate, a car, or bank account–will automatically pass to the survivor, or you may have designated a beneficiary for a life insurance policy or retirement account. However, it is still important to have a Will or a Trust for several reasons. Certain assets must pass through your estate (for example, personal objects or cryptocurrency), so the only way to direct where they go at your death is through a legal document. Having no assets in your estate will make it difficult to pay for your last expenses, including funeral costs, legal fees, and any taxes.

Who’s Involved in an Estate Plan?

Now that we’ve looked at the important reasons why to have an estate plan, it’s time to turn to the who in an estate plan.

The most important person is you, the creator of the Will (testator) or Trust (called grantor, settlor, or trustor–not to be confused with the trustee!). By taking the time for careful consideration and creating various legal documents, you are establishing clear expectations for how you want your money and property to be handled upon your death.

The other essential players involved in estate planning include:

Beneficiaries: These are family members, loved ones, or charitable organizations—anyone who receives an asset of yours in your Will or Trust. Assets can include cash, real estate, or that piano you inherited from your grandparents.

Heirs: If you die without an estate plan (or all the beneficiaries you listed in your estate plan have passed away or otherwise do not qualify to receive your assets), the people who will receive your assets are known as your heirs. Your heirs are determined under default succession laws. They are not necessarily the people you would have named as your beneficiaries.

Executor: If you create a Will, you will name an executor (sometimes called an administrator or personal representative) to manage your affairs after you die. This person will collect your property, pay any debts and taxes, and distribute the remaining property according to the terms of your Will. This often takes a bit of legwork, including contacting banks, investment and insurance companies, and appraisers.

Trustee: When the centerpiece of your estate plan is a Trust rather than a Will, this person manages your affairs just like an executor would. Because the roles are so similar, generally the same person is named in the role of successor trustee and executor. Moreover, if you put assets into your Trust during life, the trustee can manage them during your incapacity, instead of relying on a financial power of attorney.

Agent or attorney-in-fact: Not to be confused with an actual lawyer, this is the person you named in your financial or health care power of attorney to act or make decisions on your behalf.

Guardian: If you have children who are minors or have special needs, this is the person you name to care for the wellbeing in case both you and the other parent are unable to care for those children.

If you’re wondering whether a lawyer is also part of this list, it depends. Most people can set up and manage their estate plan on their own using online tools, like Wealth, which are backed by extensive legal expertise.

When you put together the what, why, and who behind estate planning, you can see it really boils down to thinking about and documenting your final wishes, then appointing someone you trust to be in charge of executing those wishes after you die. It’s a simple, thoughtful act that protects your family and your legacy.

We hope these explanations have shown that estate planning is important but not impossible. Like death itself, it’s not something people talk about much, which has led to a myth that it’s too complicated for the average person to tackle. The reality is, estate planning takes time and consideration, but it’s time well spent to safeguard your loved ones’ wellbeing.

Online options for things we once did in person are on the rise, and estate planning is no exception. Inexpensive and easy-to-use digital planning tools now allow you to create your Will, Advance Health Care Directive, and other estate planning documents at a fraction of the cost of hiring an attorney. But how do you know if digital estate planning is the right choice for you?

Below we answer common questions regarding ease of use, privacy, and security considerations when selecting a digital estate planning platform.

Q: Does the digital estate planning platform keep my information secure?

A: An online estate planning service should maintain rigorous security standards to protect user privacy. Wealth uses multi-factor authentication and bank-level encryption to secure all data from any potential breach.

Q: Is my situation too complicated for online estate planning?

A: Most online estate planning platforms work well for uncomplicated family and financial situations. The Wealth platform provides for unique situations, including blended families, gifts of specific items, creation of estate tax-exempt Trusts (e.g., the credit shelter or bypass Trust), and family-owned businesses. If you have any questions regarding your estate, you should consult a qualified attorney. Even if you’ve already created a Will or Trust with an attorney, you can still use online estate planning to modify those documents and manage your estate plan and keep track of your Trust assets.

Q: What are the pros and cons of digital estate planning?

A: Online digital estate planning can be much less expensive than meeting with an estate attorney in person. Additionally, you can revise your estate documents if you change your mind about gifts, agents, or if your life circumstances change. Digital estate documents do not include legal advice specific to your situation. If you have any questions about your estate documents, you should speak to a qualified attorney.

Q: What information do I need to get started with my digital estate plan?

A: You can start your digital estate plan by simply providing your contact information and creating an online account. Once your account has been set up, Wealth will guide you step by step through the process of adding family members, beneficiaries, assets, gifts you would like to give, etc. Wealth provides guidance on how to select trusted agents, validate documents, and alerts you when issues might arise when transferring property or giving gifts.

Q: How do I know my digital estate planning documents are valid?

A: Each state has its own laws about signing, witnessing, and notarizing estate planning documents. Wealth provides signature pages that are valid in your state of residence. Additionally, your Wealth documents will include detailed signing instructions and will alert you if a notary and/or witness(es) is required at the time of signing.

Q: I’m ready to begin my online estate plan. Why should I choose Wealth?

A: Wealth estate planning documents have been customized for the laws of your state and have been reviewed by a licensed attorney in your state.Wealth uses multi-factor authentication and bank-level encryption to secure your data from any potential breach. You can revise your documents at any time on your Wealth Portal online account. For an additional fee, an attorney licensed in your state is available to answer questions specific to your estate needs.

Ready to begin creating your estate plan? Click here to get started.

So much of estate planning is thinking through how you want things handled after you die, before you start actually making a documented plan. The idea of a financial power of attorney (FPoA) flips that a bit, because it’s about appointing someone to handle your affairs in case you become incapacitated and can’t make your own decisions. The process seems complex, but we’ll simplify it so you can make sense of the basics you need to know to include this important element in your estate plan.

What Role Does a FPoA Play in Estate Planning?

In a nutshell, a financial power of attorney is a document in which you appoint a trusted person to act on your behalf to make financial decisions. In establishing a FPoA, you hand over the legal reins to another person to conduct financial transactions, sign documents, or make other legal decisions as if they were you. This might happen for only a limited period of time (during a serious illness or after an accident, for example), or it can take effect immediately upon signing and last up to your end of life. Once your FPoA is completed, your trusted person, the agent, sometimes called an attorney-in-fact or fiduciary, can be responsible for managing your financial affairs. You will need to use a second document, called an Advance Health Care Directive (sometimes known as health care proxy or health care power of attorney), to designate who should handle all of your medical decisions. There are several types of FPoA, so consider the specific needs of your estate before selecting one.

Durable Power of Attorney

The type of FPoA most commonly used in estate planning is a durable power of attorney. “Durable” indicates that your agent has your permission to act on your behalf even though you are incapacitated or disabled. In other words, the FPoA is effective until you either revoke the document or have passed away.

You can spell out your agent’s powers, responsibilities and restrictions in the FPoA. The powers vary from state to state but usually include the ability to:

Sell or manage property and real estate

Sign legal documents and checks

Manage personal and business-related financial accounts

Pay medical bills (but not make healthcare decisions)

File taxes and settle claims on your behalf

Hire professional assistance, such as a lawyer or advisor

Non-Durable Financial Power of Attorney

When an FPoA is not “durable,” your agent’s powers end when you become incapacitated or disabled. In other words, you want to supervise your agent’s use of the FPoA powers. This can be a good option for transactions that are not driven by estate planning needs. For example, you might grant your advisor a non-durable FPoA to conduct time-sensitive trades on your behalf.

In addition, you may be comfortable allowing your agent to change your estate plan or the rights of your beneficiaries; because these are such sensitive powers, in most states, you must affirmatively grant each estate planning power.

Why Include a Durable Power of Attorney in Your Estate Plan?

A complete estate plan should provide not only for death, but incapacity and unavailability. Putting a FPoA in place allows someone to continue managing your financial affairs if you cannot sign important documents yourself in case of emergency, a routine surgery, or even travel abroad.

Keep in mind that to complete your FPoA, it must be signed in accordance with your specific state’s requirements, which might mean signing before a notary public or witness(es).

The wealth.com platform makes it straightforward to get your Financial Power of Attorney drafted and securely stored in our Vault, and provides state-specific guidance on how to fill out and sign your FPoA.

Get this guide to Financial Power of Attorney as a printable PDF

To continually deliver quality and value to our members, we take a proactive approach to product innovation. This update highlights features from the month of April. We welcome any feedback or questions: [email protected]

New Feature Spotlight

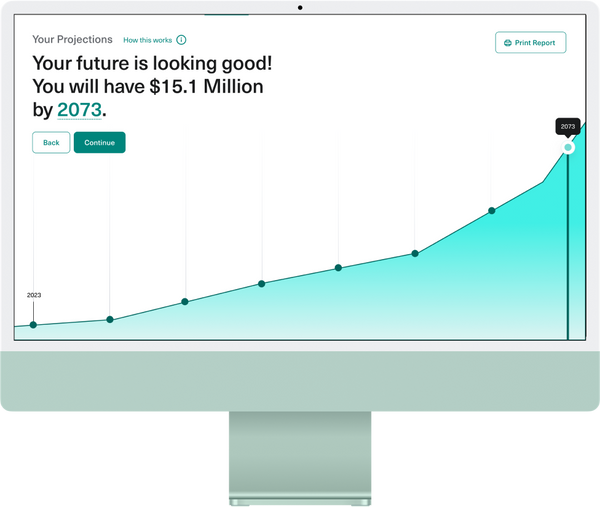

Our Wealth Projections Calculator is now live. Going beyond comprehensive net worth calculations, our machine-learning-based model projects a member’s future net worth, the potential impact of federal estate taxes on their taxable estate, and what their beneficiaries may receive based on these insights. Designed by the SVP of Machine Learning, the former Head of Data Science and Machine Learning at Vanguard, our proprietary machine learning model uses specific asset types to provide realistic projections, relying on 20+ years of economic data customized specifically to capture signals that might impact a member’s net worth.

Interested in exploring the Wealth Projections tool?

We further customized our document creation workflows to accommodate members who are in long-term, but not legally-recognized relationships, so that they can better document their wishes to include their long-term partner. This includes an analysis of how this relationship status impacts tax and estate planning based on federal laws.

Revocable Trust and Last Will & Testament documents now allow members to choose to redistribute a deceased beneficiary’s shares among other chosen beneficiaries, or to instead pass the shares to the deceased beneficiary’s descendants.

In order to help create legally sound and accurate documents, we enhanced our document creation workflow to guide members to sections of their drafting that may warrant an additional review.

For Financial Advisors

Our advisor partners and their relationships with their clients are extremely important to us. We updated our onboarding experience to improve clarity on the relationship between the client and advisor, highlighting that the platform does not enable the advisor to provide legal advice to the client.

To improve efficiency and streamline onboarding, we added flexibility to the client invitation process for advisors by enabling the ability to copy a link to invite their clients to join Wealth.

With recent banking volatility, highlighted by Silicon Valley Bank falling under FDIC receivership, asset protection is top of mind for advisors’ clients. In response, we released new content for advisors to leverage in conversations with their clients, including how effective estate planning can be used as a tool for asset protection and FDIC coverage.

Additional Updates

The onboarding experience was updated to reflect more specific details, including if a member has children and/or already has an estate plan, to provide more personalized experiences in app and smarter auto-completion within the document creation workflows.

We want to hear from you. Please share your feedback with us!

A Trust is a financial agreement between someone who owns an asset and a trusted person to hold and manage that asset for them. In estate planning, a Revocable Trust is often used as a substitute for a Will, but there are many types of Trusts that accomplish different objectives. If you’re trying to decide whether you should have a Trust in your estate plan, read this two-part article.

What’s the difference between a Marital Trust and a QTIP Trust? Are Bypass Trusts and Credit Shelter Trusts trying to accomplish the same goals? As you start learning about Trusts, you’ll learn that there are subtle differences between the Trusts that you might include in your foundational estate plan. Adding to the confusion, each lawyer has a different name for Trusts that do pretty much the same thing, and we try to provide the most common names for them.

Choosing to use a Trust in your estate plan is about being clear on your goals for how your assets should go to your loved ones. Trusts are created through a contract, and so there are a million different ways to write a contract to meet your specific goals.

This Article is divided into two parts. Part 1 is a primer on the key differentiators between Trusts. This Part 2 is a summary of the most commonly created Trusts in a foundational estate plan and their benefits.

The trusts named in this article are the ones you are most likely going to encounter when creating your foundational estate plan, which is centered on a Will or Revocable Trust and disposes of your assets when you pass away. This article does not discuss Trusts that you might create during life for wealth transfers or tax planning.

It is also important to realize that the descriptions for these Trusts are not mutually exclusive; you can use multiple adjectives to describe one Trust in your estate plan. For example, you can create a Marital Trust that is also a Spendthrift Trust.

Revocable or Living Trust

This Trust is most often used as an alternative to a Will for disposing of someone’s assets at death. It is also a great vehicle to transition the management of your financial affairs smoothly to someone whom you trust, in case you become incapacitated.

Learn more about Revocable and Irrevocable Trusts in Part 1 of this article.

Marital Trust

The Trust’s creator (“trustor”) creates this irrevocable Trust for the primary benefit of the spouse (i.e., your spouse can enjoy your assets after you have passed away). A Marital Trust is useful for someone who has a blended family, worries about elder abuse of their spouse or someone influencing their spouse to disinherit their beneficiaries, or is wealthy enough to worry about the estate and generation-skipping transfer taxes. There are many ways to design a Marital Trust, but if you also want your spouse’s inheritance to qualify for a benefit called the “unlimited marital deduction” (i.e., you could pass an unlimited amount of property to your spouse completely free of estate tax at your death), the Tax Code has stringent requirements for the design of this Trust (see “QTIP Trust” below).

QTIP Trust

The Qualified Terminable Interest Property Trust is a specific kind of Marital Trust. Its terms are properly structured to comply with the tax rules so that you can pass your property to your spouse in a trust and still benefit from the unlimited marital deduction.

One of the biggest “loopholes” under the estate tax rules is the unlimited marital deduction. This deduction allows you to pass unlimited amounts of property to your spouse (beyond the estate tax exemption of $12.92M in 2023), completely free of the estate tax.*

Not all Marital Trusts comply with these rules. For example, your Marital Trust may say that your spouse will be the only beneficiary for the rest of your spouse’s life, but if your spouse remarries, the Trust will end and your assets will pass to your other loved ones. By inserting the condition about remarriage, your Marital Trust does not comply with the tax rules. Your gift to your spouse counts toward the federal tax exemption, along with any property you pass to other non-charitable beneficiaries, and could lead to an inadvertent foot fault where your estate owes estate taxes.

____

*As with all things tax, there are a lot of factors to unpack in this statement. Importantly, your spouse must be a U.S. citizen. In addition, the federal government only grants this benefit to individuals who are legally married, and not individuals in a domestic partnership, civil union, or other relationship arrangements. The fact that the unlimited marital deduction was not available for individuals in same-sex marriages performed under state law was the basis for the seminal case, U.S. v. Windsor, 570 U.S. 744 (2013). The case declared the federal law, the Defense of Marriage Act, to be unconstitutional and forced the federal government to grant the same government benefits to same-sex spouses. Those government benefits include the estate tax deduction!

Family, Bypass, or Credit Shelter Trust

This Trust goes by many names, but in essence, it is an irrevocable Trust created at your death to allow your family to engage in death tax planning.* If your estate may have a tax issue, this Trust allows your executor or trustee to use what remains of your tax exemption amount ($12.92M in 2023 at the federal level*2) and shelter those assets from future death taxes. This Trust becomes a “family bank,” where assets continue to grow and benefit a family, but no death tax will be imposed with the passing of each generation.

____

*“Death taxes” in this article refers to the estate tax and generation-skipping transfer tax. These two tax regimes exist at the federal and state levels.

*2 The exemption amount may be significantly lower at the state level, and can be as low as $1M.

A/B Trusts

This term applies to estate planning for couples. It describes the most common combination of Trusts that are formed at the death of the first person who passes away: the Marital Trust (“A Trust”) and the Family Trust (“B Trust”). Your estate plan will then specify a mechanism for how your executor, trustee, or even your spouse, can allocate assets between those two Trusts.

As an additional variation on this term, if you and your spouse have a joint Trust (i.e., you created your estate plan together through one Revocable Trust), your estate plan may use A/B/C Trusts. In addition to the Marital and Family Trusts, your estate plan might create a Survivor’s Trust (read more below).

Survivor’s Trust

The Survivor’s Trust is relevant only when a couple creates a joint revocable Trust; it is the continuation of the revocable Trust once one person has passed away. With a joint Trust, the estate plan must describe where all of the couple’s assets will go – not only the deceased person’s assets, but also the survivor’s assets. Because one half of the couple is still living, the Survivor’s Trust exists to collect and hold the survivor’s assets without requiring the survivor to create a brand-new estate plan. The survivor can thus change and revoke the Survivor’s Trust as desired (but a Marital Trust or Family Trust is irrevocable).

Trust for Descendant or Trust for Issue

This type of Trust goes by many names, and often references the name of the primary beneficiary (e.g., Trust for Sara). This irrevocable Trust allows the beneficiary to enjoy the Trust assets, but without the full control that comes with owning assets in their own name. This Trust is useful for designating someone else to manage financial affairs while the beneficiary is not ready or able to handle the responsibility, ensuring that assets stay within a family, protecting an inheritance from divorce or creditors (e.g., the beneficiary’s personal debts), and planning for death taxes.

These Trusts are drafted in many different ways, and can take the form of a Holdback Trust or Special Needs Trust, as appropriate.

Holdback Trust

The primary purpose of this Trust is to “hold back” the inheritance for a younger beneficiary until the beneficiary comes of age. This irrevocable trust is meant to be a temporary vehicle and is more robust than a UTMA account in allowing the trusted person to manage the beneficiary’s finances. Usually, you will be given the opportunity to decide on which birthday the trust will end and the beneficiary should be able to receive all the assets.

Special Needs Trust

This irrevocable Trust is structured with a beneficiary who has long-term special needs in mind. The Trust usually lasts during the life of the beneficiary and preserves the beneficiary’s eligibility for government programs like Medicare. This Trust should have provisions allowing a trusted person to modify the Trust terms to optimize the Trust for the needs of that beneficiary, such as restricting certain powers, or adapting to government rules to access benefits.

Charitable Trust

This irrevocable Trust benefits a charity, and usually is created so that the gifts to the Trust qualify for a charitable deduction for income tax purposes, estate tax purposes, or both.

The second of the biggest “loopholes” in the estate tax rules is that a properly made gift to charities qualifies for an unlimited deduction (see “QTIP Trust” for the other unlimited deduction). To set up a Charitable Trust for tax planning, you must make sure that there are restrictions so that the organization cannot receive a Trust distribution unless it qualifies under the Code (usually, an organization that has maintained its 501(c)(3) status, but the estate tax rules have slight variations).

Pet Trust

This irrevocable Trust benefits pets. You would name someone to take care of the pets and to handle the finances for your pets (which may be the same person or different people). However, Pet Trusts are disfavored under the law. For example, you may be able to benefit only the pets who are alive when you pass away, and not their descendants, and the Trust’s distributions are taxed as income to the caretaker even if they are used to cover the pets’ expenses.

Spendthrift Trust or Asset Protection Trust

This Trust must be properly structured according to state law to grant the layer of protection from legal claims against the beneficiary and the creditor’s state must also respect that result. When the asset protection is respected, the Trust’s assets are considered separate from the personal assets of the beneficiary to satisfy personal claims against the beneficiary. For example, the Trust’s assets may not be considered in alimony calculations upon divorce, or the Trust’s assets cannot be forced out of the Trust to pay the debt or a monetary judgment against the beneficiary. Oftentimes, creating this Trust requires an affirmative statement in the Trust document and giving the trustee full discretion to decide when distributions can be made.

A Trust is a financial agreement between someone who owns an asset and a trusted person to hold and manage that asset for them. In estate planning, a Revocable Trust is often used as a substitute for a Will, but there are many other descriptions for any single Trust such as Irrevocable, Living, Joint, Testamentary, and Grantor. If you’re trying to unpack these terms and decide whether you should have a Trust in your estate plan, read this two-part article.

A Joint Trust, a Testamentary Trust, a Sub-Trust, a Revocable Trust (which sounds so much like “Irrevocable Trust” when said out loud)… There are so many adjectives used to describe Trusts, and it can quickly make your head spin. Once you dig deeper into these descriptive words for Trusts, you realize that many of these concepts come in pairs. Once you understand what feature of a trust is being described, and what the point of comparison is, it becomes much easier to understand the Trust’s use case.

This Article is divided into two parts. This Part 1 is a primer on the key differentiators between Trusts. Part 2 is a summary of the most commonly created Trusts in a foundational estate plan and their benefits.

Choosing to use a Trust in your estate plan is about being clear on your goals for how your assets should go to your loved ones. Trusts are created through a contract, and so there are a million different ways to write a contract to meet your specific goals.

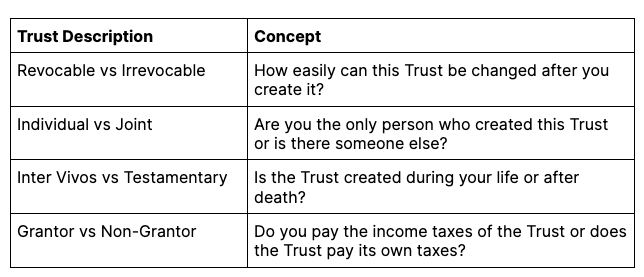

Here are the ways to describe a Trust that we will explore in this article:

Every term describes a different aspect of a Trust, and they are not mutually exclusive. In fact, every Trust can be described using one of the two choices from each category above. For example, if you use a Trust as a substitute for a Will in your foundational estate plan, you likely created a Revocable, Individual, Inter Vivos, Grantor Trust (most commonly shortened to “Revocable Trust”). If a Marital Trust will be created at your death, you will be creating an Irrevocable, Individual, Testamentary, Non-Grantor Trust. Let’s unpack each of these terms.

Revocable vs Irrevocable Trusts

The Revocable Trust, as the name implies, can be undone or unwound; the person who creates the Revocable Trust can simply “revoke” or “pull back” the Trust. The Irrevocable Trust, on the other hand, is much harder to change.

The Revocable Trust is often used as an alternative for a Will. It can also be used as an alternative to LLCs or Corporations to own an asset more privately while the owner is still alive.

The Irrevocable Trust is often used to give away assets while maintaining control over how the assets are used or to protect from specific types of taxes.

For most people, the introduction to Trusts begins with their own estate planning when they have to choose between making a Will or a Trust. In this context, the type of Trust you will be considering is the Revocable Trust (also commonly called a “Living Trust”).*2

Just as you would be able to change or completely revoke a Will (in many states, you could do this by ripping the original document!), you should be able to change or completely revoke your Revocable Trust. This is important because you could change your mind over the course of your life about key terms, such as who should get what asset. While you are alive and have mental capacity, you can easily change or revoke your Revocable Trust by signing a new Trust document.

An Irrevocable Trust is much harder to change, and it becomes especially difficult to remove or add beneficiaries or modify their individual rights. You might encounter this type of Trust even when creating your foundational estate plan (for example, a Marital Trust). In most states, once the Irrevocable Trust exists, changing this Trust requires the appointment of an independent trustee (if the Trust allows for it), the agreement of all the beneficiaries, or a court action. All of these options may be expensive and may require hiring an estate planner to do it right. For this reason, you must be certain you understand what powers and benefits you are giving up when you transfer property into an Irrevocable Trust.

That being said, Irrevocable Trusts are powerful vehicles for wealth transfer and preservation because you can control how the assets will be used. When properly structured, they provide protection against death taxes and creditors, which Revocable Trusts cannot do.

___

*This article is about different adjectives describing Trusts. To learn more about why you would want a Revocable Trust instead of a Will, check out the article.

*2 “Living” is also sometimes used interchangeably with “Inter Vivos” (see section on “Inter Vivos v. Testamentary Trusts”). But its most common use is to mean a Revocable Trust that is used as a substitute for a Will.

Individual vs Joint Trusts

An Individual Trust has one creator (called a “trustor,” “grantor,” or “settlor”), whereas a Joint Trust has two or more trustors. If you would like to create a Trust with someone else, be clear on why.

The most common reason to set up a joint trust is with your spouse. You already share in the management of the assets (e.g., you live in a community property state), file income taxes together, and share similar values, goals, and beneficiaries.

Income tax filings and payments may become messy if you and the other person are expected to report and pay the income taxes on the assets of the Trust (see “Grantor vs Non-Grantor Trust”) below.

For gift tax reasons (as well as introducing potential for complicated legal claims), you should also consider carefully giving your assets into a Trust that was created by someone else. For example, it may be tempting to give an inheritance to your nephew in a Trust that your parents set up for your nephew. It may be better for you to set up your own Trust to keep the Trust management straight-forward.

Inter Vivos vs Testamentary Trusts

Inter Vivos Trusts* are created during the trustor’s lifetime, whereas Testamentary Trusts are created only at the trustor’s death. This description is about the timing of when a Trust exists and can hold assets.

Inter Vivos Trusts allow the creator of the trust to transfer assets during life. Testamentary Trusts lie in wait until the creator has passed away and receive assets only then. The most common way to create a Testamentary Trust is to draft it into a Will or within another Trust (i.e., a “Sub-Trust”).

You may encounter both Inter Vivos and Testamentary Trusts when creating your foundational estate plan. For example, if you use a Revocable Trust as a substitute for a Will, you are creating an Inter Vivos Trust. In fact, it is important to transfer as much of your assets into this Trust during your life, if minimizing probate is important to you.

Your estate plan may also involve any number of Testamentary Trusts (created under your Will or your Revocable Trust) in order to specify how your assets can be used or given away after your death or to allow your loved ones to minimize future taxes. For example, you might set up a relatively short-lived Testamentary Trust called a “Holdback Trust” just so someone can help your child manage their financial affairs until your child is older.

____

*This term means “among the living” in Latin, and the English translation is “Living Trust.” However, the Living Trust is now commonly associated with Revocable Trusts used as a substitute for a Will, and so “Living” has become a confusing term because you can create an Irrevocable Trust during your life.

Grantor vs Non-Grantor Trusts

If you’ve made it this far in this article, you are really well on your way to understanding the features of a Trust that are important to an estate planner. Here is one more concept, which may matter more to your CPA. Your Trust may own assets that produce income (for example, real estate that is leased). It’s important to understand who is responsible for paying income taxes for Trust assets: you or the Trust.

A Grantor Trust does not pay its own taxes; another person (usually the Trust creator) must include the Trust’s income on his, her or its tax return and pay any income taxes. A Non-Grantor Trust pays its own taxes using the tax brackets for estates and trusts, which are different from the tax brackets for individuals.

Grantor Trusts retain enough of a connection to its “owner” (or “Grantor”) under the Tax Code so that the Grantor pays the taxes. Who is an owner is determined under a complex set of tax rules, and estate planners often intentionally turn on or turn off Grantor status on the Trust; but at a minimum, the owner must still be alive.

Having a Grantor trust is beneficial if you do not want to complicate tax reporting by having the Trust file a separate tax return or you want to treat the payment of taxes as an additional annual gift to your loved ones. In addition, a Non-Grantor Trust generally pays more income taxes than an individual taxpayer on the same amount of income. This is because the trust tax brackets are “compressed”; a Trust taxpayer reaches the maximum tax rate (i.e., 37%) at a lower income than does an individual taxpayer.

How does this concept apply to your foundational estate plan? If you use a Revocable Trust as a substitute for a Will, it will be a Grantor Trust that you “own” during your lifetime. A Revocable Trust does not result in any income tax savings: you must include the Trust’s income on your own tax return and pay those income taxes.

If you use a Sub-Trust (or Testamentary Trust) in your Will or Trust, that Trust will be created at your death and will usually be a Non-Grantor Trust. It will have to file and pay its own income taxes.

If you’re ready to get started creating a Revocable Trust follow this link.

To learn more about specific types of Trusts and their objectives, read Part 2 of this series.

What’s the Difference and Which One Is Right for Me?

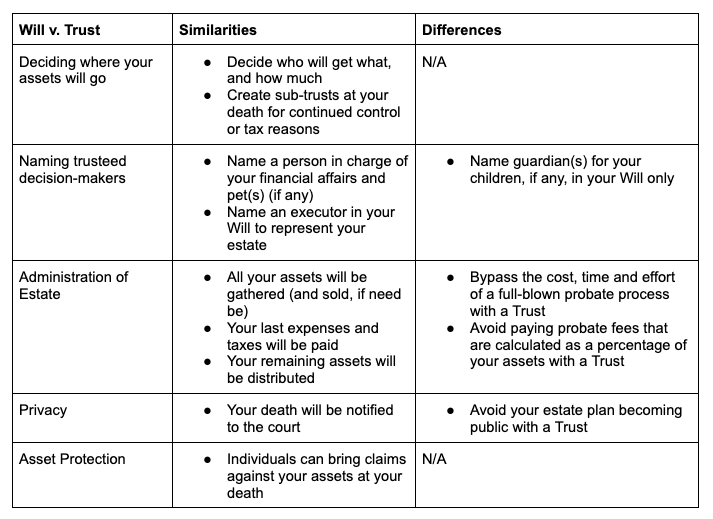

TL/DR: In simple terms, a Will is a legal instruction to the court about what should happen to what you own after you have passed away. A Trust is a contract you make with someone whom you trust about what you own, regardless of whether you have passed away. There are many types of Trusts, but the Revocable Trust (or Living Trust) is most commonly used as a substitute for a Will. The Revocable Trust may offer you some advantages that a Will doesn’t, as this article will explain.

In climactic movie scenes and music videos when a family gathers to hear how the dead person’s fortune will be split up, it’s always the deceased’s Will being read out loud for the big reveal. In real life, however, a Will doesn’t get read out loud; instead, the executor sends a copy to all known beneficiaries.

Even without a dramatic reading, you might still have concerns about keeping your last wishes private. A Will becomes a publicly available document on the probate court’s docket. Probate is often how the press learns the details of a celebrity’s assets and who the heirs are after the celebrity has died.

If maintaining your privacy is important to you, consider making a Trust – and not a Will – the centerpiece of your estate plan.

A Revocable Trust (or Living Trust)* can be a great alternative for many reasons, beyond privacy. These fall into four main categories:

Avoiding the court process at death

Keeping your wishes private

Planning for your incapacity

Learning a new set of words

Note that just because most Americans have a Will* and not a Trust does not mean that you should have a Will. Depending on your situation and wishes, a Revocable Trust may be the best option for you.

If, after we dig deeper into each of the differences, you’re still not sure, take our quiz here.

_____

*1 The rest of this article may refer to this type of Trust as simply “Trust.” A Revocable Trust (or Living Trust) is not to be confused with an Irrevocable Trust. Learn more about this topic here.

*2 A lot more people have a will (60% of the people we surveyed in our estate-planning research who have an estate plan) vs. a trust (38% have a living or revocable trust, and just 19% have an irrevocable trust).

Avoiding the Court Process at Death

The main reason people choose a Trust is to simplify the court process that happens at death, which is called “probate.” If you die with a Will that distributes your assets (or without an estate plan at all), a probate judge will oversee how your assets will be distributed.

This process can be difficult and expensive and take a long time. If one or more factors indicate that probate will be more onerous for your estate, you should consider putting in place a Trust to avoid probate. These factors are:

(a) You live in a state that tends to have a complicated or expensive probate process.

(b) You own real estate (or tangible objects of significant value) that is located in a state other than your home state.

(c) You own assets that are complex and may require more active court supervision, like stock that is not publicly traded.

Unpacking each of these factors:

(A) Some states charge probate or court fees based on the size of your estate (i.e., how much you owned in your name at death). Attorneys may charge up to tens of thousands of dollars to help your executor navigate probate. All those fees are first paid from your assets, so there will be less left to distribute among your loved ones. And even when your assets are not particularly complex, probate in your home state could tie up your assets for up to two years. If you live in a state like this, a revocable trust will allow you to put more control in the hands of your trustee and “bypass” much of the probate process.

(B) If you own real estate or personal property in another state, dying with only a Will means that your executor must start probate processes not only in your home state, but in all the other states as well. By putting the property located in other states in your revocable trust,* your trustee will be able to avoid these “offshoot” probate proceedings.

(C) If you own assets that are a little more complex, such as stock that is not publicly traded, your executor will have to coordinate more closely with the probate court to make sure the stock is properly transferred to the appropriate beneficiaries. This can lengthen the time for probate.

If you anticipate that probate would be costly and time-consuming for your loved ones, a Revocable Trust might be the best option for you.

____

*If you place the real estate or personal property in an entity like a limited liability company (LLC), you may also be able to avoid probate, but that analysis must be done by an attorney licensed to practice law in the state where your real estate or personal property is located.

Keeping Your Wishes Private

As part of the probate process, a Will becomes part of the public record. Revocable Trusts typically avoid probate (unless there is an issue like an angry family member who brings a legal claim against your Trust). With a Revocable Trust, your estate plan is more likely to remain private.

Information that will become public if part of your Will include:

(a) Who you consider to be your family members.

(b) Who you want to exclude from receiving your assets or having a trusted role in your estate plan.

(c) Who will receive your assets, and how much of your assets they will receive.

(d) How you would like your last remains to be handled.

If you would prefer to keep these details private, a Revocable Trust might be the best option for you.

When They Become Effective

A Will does not become effective until you die, whereas a Trust is effective immediately on the day you create it. As a result, a trust has legal effect before your death – i.e., while you are alive but either incapacitated or unavailable. If it is important for you that someone take over responsibility for your financial affairs immediately if something were to happen to you, then a Revocable Trust gives you a more powerful vehicle compared to a Will or a financial power of attorney.

Ensuring that “it’s business as usual,” can be especially important if you own a closely-held business and you are expected to be involved in the day-to-day operations or in making high-level decisions by voting your shares. Your succession planning for your business should include transferring your shares into a Trust so that your trustee can step into your shoes if something happens to you.

Learning a New Set of Words

A Trust can be used as an alternative to a Will, but the vocabulary will be different and less familiar to most people, which contributes to the feeling that Trusts are more complicated than Wills. For example, instead of referring to an “executor” or “personal representative,” the trusted individual who will manage your affairs is called a “trustee.”

That being said, if there are factors indicating that you should have a Revocable Trust, you should not let legal terms discourage you from using a Trust as the centerpiece of your estate plan.

What Are Common Misconceptions about What a Trust Can Do For Me That a Will Can’t?

1. If you have a Revocable Trust, you won’t need a Will.

Even if you have a Revocable Trust, you will still need a Will. If you pass away with any assets in your own name, you need a Will to make sure all of those assets go into your Trust, where the Trust will instruct where those assets will go. This type of Will, which accompanies a Revocable Trust, is much shorter than a standalone Will and is commonly known as a “pour-over Will.” This is important because some assets must be owned in your own name while you’re alive, like a retirement account, and you may not get around to putting all your assets in the name of your Trust before you pass away.

You will also need a pour-over Will to name an executor and guardian(s) for your children, if any.

2. As long as I have a Revocable Trust, my loved ones will definitely avoid probate.

A Will must go through probate, whereas a Revocable Trust has the opportunity to avoid probate.

First, you will need to “fund” your Trust, which means transferring as much of your assets as possible into your Revocable Trust. Some courts, like in California, may allow you to avoid a full-blown probate if you show that you intended to fund your trust by signing a general assignment of all your assets into the trust. Other states will instead require that you actually re-title any real estate and change the owner on your bank accounts and other assets.

Lastly, the probate court may become involved to resolve any issues among your beneficiaries or trustees. For example, someone may call into question whether your Will and Trust are not valid.

3. A Revocable Trust will make it harder for someone to sue my estate.

We all fear that someone will be unhappy with the wishes of the decedent or how the estate administration is being handled and bring a lawsuit against the estate. Having a Revocable Trust instead of a Will will not deter a motivated person from suing against your assets at your death.*

Note that a Revocable Trust should not be confused with an Irrevocable Trust, which may offer some level of asset protection. Asset protection means that a creditor (for example, someone to whom the Trust beneficiary owes money for an accident) may not be able to reach the Trust assets because the assets are considered to be separate from the beneficiary and cannot be used to fulfill the beneficiary’s debt.

4. If I anticipate that my estate will owe death taxes, I must have a Revocable Trust.

Tax planning for estate and generation-skipping transfer taxes can be accomplished with either a Will or a Revocable Trust as the centerpiece of your estate plan. You do not need a Revocable Trust just because you may have a death tax issue. The important thing is to make sure your Will or Trust has the proper provisions to meet your tax planning goals. Your Will or Trust must create Trusts after you’ve passed away (a testamentary sub-Trust) that comply with the Tax Code and direct your assets into those sub-Trusts using rules or formulas that will minimize taxes in the long term.

Sub-Trusts are Irrevocable Trusts created at your death and are not to be confused with Revocable Trusts that you create while you are alive as an alternative to writing a Will.

5. If I would like more control over how my assets are used after my death or keeping my assets within my family across generations, I must have a Revocable Trust.

If you would like to maintain some control over how your assets are used or gifted away after your death, you should make sure sub-Trusts (see 4 above) are created after your death. To create this type of sub-Trust, you can use either a Will or a Revocable Trust as the centerpiece of your estate plan.

Sub-Trusts are Irrevocable Trusts created at your death and are not to be confused with Revocable Trusts that you create while you are alive as an alternative to writing a Will.

____

*Certain estate planning tools exist to deter someone from suing your assets, including “no contest” or “in terrorem” clauses. These tools can be implemented in a Will or a Trust with the advice of an attorney.

The chart below summarizes the overlap and differences between a Will and a Revocable Trust in most U.S. states.