Estate planning isn’t just about what happens after you die. It’s also about knowing how to best pass on your wealth during your lifetime, especially your children.

In this episode, hosts Thomas Kopelman and Dave Haughton discuss different ways to play for your children’s future. They explore various types of accounts, including UTMA accounts and 529 plans, detailing the pros and cons of each. They also discuss gifting, including how to help with large expenses like student loans and housing, and when to utilize trusts.

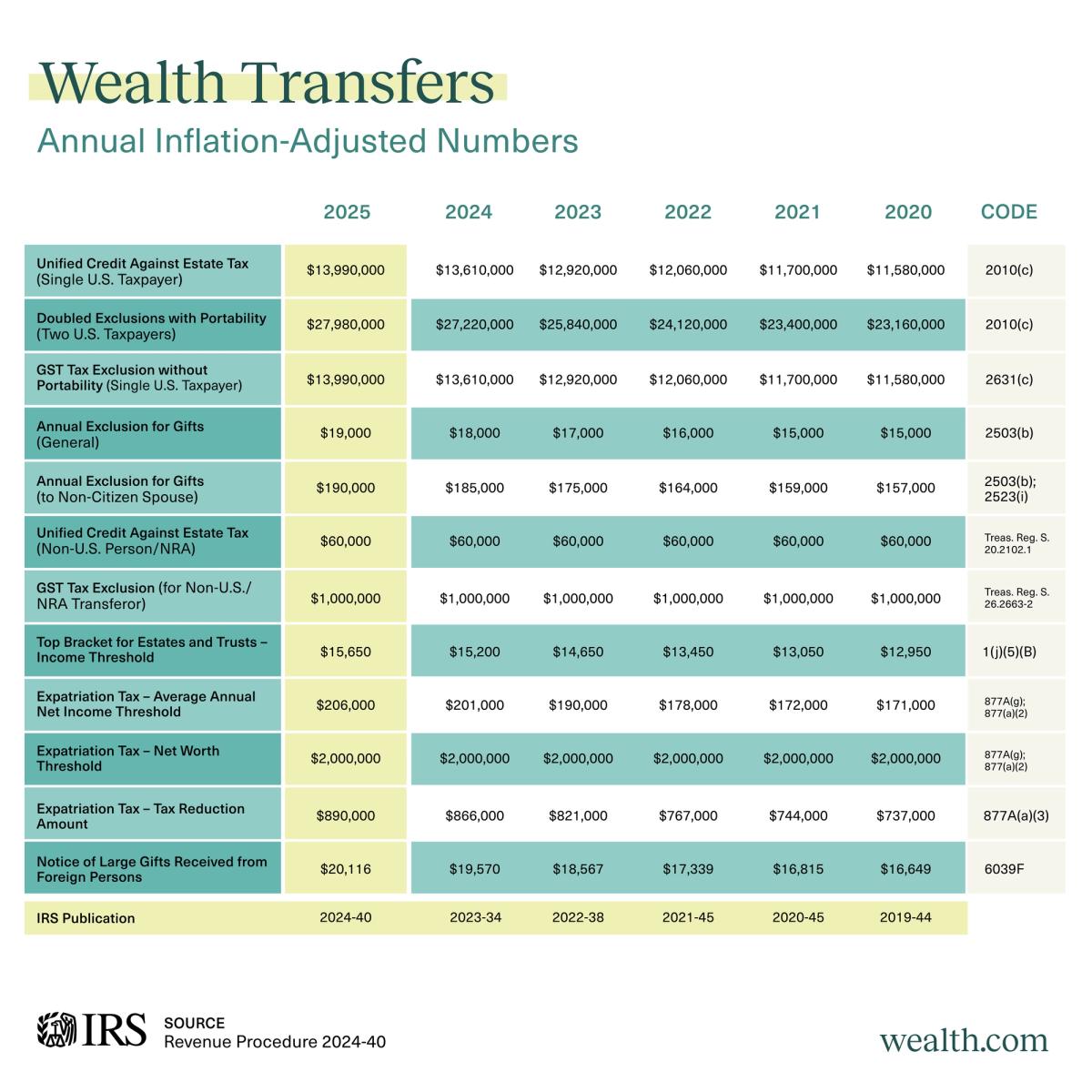

The IRS just released its 2025 numbers adjusted for inflation. These can have a significant impact on wealth and estate planning.

For many people, the major take away is that the annual gift exemption is increasing to $19,000. For those that already have a gifting strategy or plan significant gifts in 2025—such as contributing to tuition or a down payment for a family member—this increase can help with certain tax strategies.

The other takeaway is the lifetime estate and gift tax exclusion is increasing to $13.99 million for individuals and $27.98 million for married couples, which applies to clients that have high-net worth estates. In 2025, this is even more significant because the Tax Cuts & Jobs Act (TCJA) is set to sunset at the end of the year. Unless Congress extends the provisions in the TCJA, the estate and gift tax exclusion will return to pre-2018 numbers—adjusted for inflation, it would likely be at just under $7 million for individuals.

That’s why it’s for critical for financial advisors to review these 2025 numbers alongside your clients’ plans to understand if there is any impact or opportunities for new estate tax strategies next year.

We reviewed Revenue Procedure 2024-40 and pulled out only the relevant numbers for wealth planning to provide advisors, and their clients, a simple reference chart. View it below or download a version that you can keep handy.

Actionable takeaways & impacts

While the impact of these wealth transfer-relevant numbers on your clients’ estate plans will depend on their financial situation—for example, individuals with taxable estate well under $13.99 million are likely to be unaffected by the lifetime exemption—there are potential strategies you can employ for those that could be impacted.

Here are some examples of how you can use these numbers to create a strategy for affected clients in 2025:

1. Maximize lifetime wealth transfer

Your clients can now contribute significantly to irrevocable trusts and/or make substantial gifts without incurring taxes due to the increase in the lifetime estate and gift exemption to $13.99 million for individuals and $27.98 million for married couples.

This allows you and your clients to optimize their estate planning strategies, especially if they expect to be impacted by the TCJA sunset at the end of 2025.

2. Monitor taxable gifts

Next year, the annual gift tax exclusion is increasing to $19,000. This means your clients are able to give even more without triggering gift tax. Only anything above that amount will start to impact their lifetime exclusion.

If a client already has a gifting strategy in place, for example providing gifts to their grandchildren every year, make sure they know that they are now able to increase their non-taxable gifting amount.

You should also ensure that you’re helping them track their gifting amounts. If they exceed the $19,000 they will need to file a Form 709 to report taxable gifts.

3. Leverage 529 plan contributions

Due to the annual gift tax exclusion increase, clients can now contribute up to $95,000 to a 529 plan in a single year by utilizing the five-year election option.

This can be beneficial for your clients that are looking to superfund their children’s or grandchildren’s education funds without incurring fit taxes.

4. Evaluate trust tax implications

If your clients are considering irrevocable trusts, you should assess who will be the taxpayer for the trust (i.e. is it a Grantor Trust).

This evaluation helps your clients weigh potential estate tax savings against higher income taxes, providing a clearer financial picture for them.

5. Understand non-resident alien tax implications

Be mindful of the different estate and gift tax thresholds that apply to non-resident aliens. These can have a significant impact on planning strategies.

This chart will help you navigate those complexities more effectively.

6. Address expatriation and foreign gifts

For your clients that are considering moving to a foreign country, renouncing their citizenship or green card status and/or receiving large gifts from abroad, you should be aware of the reporting requirements and tax implications.

This chart will help you quickly find the new thresholds so you can ensure compliance for your clients and avoid any penalties.

As a financial advisor, helping your clients navigate the ever-changing tax landscape is a critical part of providing comprehensive wealth management services.

One major change on the horizon is the looming sunset of many provisions in the Tax Cuts & Jobs Act (TCJA) at the end of 2025, which could have significant implications for estate planning.

With trillions of dollars expected to pass between generations in the coming years as part of the “Great Wealth Transfer,” it’s imperative that advisors understand the potential impacts of the TCJA sunset and help clients plan accordingly, especially as it relates to their taxable estates.

In this post, we’ll dive into the key aspects of the TCJA sunset, explore who’s likely to be most impacted and outline estate planning strategies advisors can explore to ensure a smooth transition for their clients.

Understanding the potential Tax Cuts & Jobs Act sunset

The Tax Cut & Jobs Act, passed in December 2017, made sweeping changes to the U.S. tax code. However, many of the provisions affecting individuals and their estates are temporary, scheduled to expire on December 31, 2025 due to the budget reconciliation process used to pass the law.

Some of the most significant provisions set to expire include:

Estate and gift tax exemption amounts reverting to pre-TCJA levels

Individual income tax rate increases

Reduction of the qualified business income (QBI) deduction for pass-through entities

Lowering of the alternative minimum tax (AMT) exemption amounts

Unless Congress takes action to extend these provisions, the tax code will revert to its pre-2018 state, which could have major ramifications for high-net-worth individuals and families and their estate plans.

Who will be affected?

The TCJA sunset will primarily impact high-net-worth individuals and families—those with assets exceeding the post-sunset exemption amounts. This may include clients who hadn’t previously needed to worry about estate taxes but have seen their wealth grow in recent years and are now in danger of surpassing the lifetime exemption amount.

Certain individuals, like business owners or those with highly-appreciated assets, may be particularly susceptible to the impacts of the reduced exemptions. Blended families and unmarried couples could also face unique challenges and may require more complex planning.

That said, even clients below the exemption thresholds should review their financial plans, as there could be state-level tax consequences to consider. Plus, life circumstances change—what may not be an issue today could become one down the road.

The biggest potential changes of the TCJA sunset

Here’s a look at some of the biggest pending changes and how advisors can prepare.

Estate & gift tax exemption: Use it before you lose it

Perhaps the most talked-about aspect of the TCJA sunset is the impending reduction in the lifetime estate and gift tax exemption. Currently, individuals can transfer up to $13.99 million ($27.98 million for married couples) in their lifetime without incurring federal estate or gift taxes due to the TCJA. It’s important to clarify that this lifetime exemption amount is separate from the annual gift tax exclusion, which allows individuals to gift up to $19,000 per recipient in 2025 without counting towards their lifetime exemption.

But this historically high lifetime exemption means that currently, only a small amount of estates are subject to federal estate tax.

That could change dramatically in 2026, when the exemption is set to drop back down to around $7 million per individual, adjusted for inflation. Suddenly, many individuals who didn’t have taxable estates will be at risk of owing substantial estate taxes, ranging from 18% to 40% on the value exceeding the exemption amount.

This potential change is most relevant to clients who have been relying on elevated exemptions for their estate plans—those with substantial wealth and assets to pass down. Advisors need to be proactive in developing strategies to minimize estate tax exposure, which could include:

Gifting appreciating assets: Clients can take advantage of the current exemption by gifting appreciating assets, like stocks or real estate, to irrevocable trusts or directly to beneficiaries. The IRS has confirmed there will be no clawback for gifts made under the current exemption, even if the exemption is lower at the time of the donor’s death. This allows clients to remove asset appreciation from their taxable estates.

Spousal Lifetime Access Trusts (SLATs): For married clients hesitant about giving up access to gifted assets, SLATs can provide a solution. One spouse funds an irrevocable trust for the benefit of the other, using their gift tax exemption. The beneficiary’s spouse can still access the funds if needed, offering flexibility and peace of mind.

Grantor Retained Annuity Trusts (GRATs): GRATs allow clients to transfer assets to an irrevocable trust while retaining the right to receive annuity payments for a set term. If structured properly, appreciation beyond the IRS Section 7520 rate passes to beneficiaries tax-free at the end of the term.

Charitable giving: The TCJA also raised the charitable deduction limit. Taxpayers who itemize can deduct up to 60% of their adjusted gross income—previously they could only deduct up to 50%. Clients who are considering a large charitable donation as part of their estate plan may want to act now before the limit reverts.

It’s important to weigh the trade-offs of these strategies. Gifting to irrevocable trusts can create long-term estate tax benefits, but advisors must carefully evaluate potential drawbacks. Relinquishing control and losing the step-up in basis at death could result in a substantial capital gains tax burden for heirs if the exemption doesn’t ultimately drop as expected or the client’s wealth ends up below the threshold.

Changing income tax rates could impact estate planning decisions

In addition to estate planning considerations, the TCJA sunset will impact clients’ income tax pictures. Tax rates are scheduled to increase across the board, with the top marginal rate rising from 37% to 39.6% and most brackets seeing a lowering of their income thresholds.

Here’s a closer look at how individual tax brackets will change:

After the TCJA sunset, more individuals and married couples will find themselves in higher tax brackets. Depending on their overall financial picture, it might make sense for certain clients to incur taxes at today’s lower rates for the later benefit of their beneficiaries.

For clients in these affected brackets, advisors may want to explore strategies to accelerate income recognition while rates remain relatively low. Options to consider include:

Roth conversions: With tax rates poised to rise, Roth conversions become increasingly attractive. By converting pre-tax retirement accounts to Roth IRAs, clients pay tax on the converted amount now in exchange for tax-free withdrawals later. This can be especially smart for clients who expect to be in a higher bracket in retirement.

Harvesting capital gains: Clients sitting on highly appreciated assets may benefit from selling and recognizing gains before rates increase. Advisors can help clients identify opportunities to strategically offset realized gains with available losses.

Accelerating business income: Business owners expecting strong profits in the coming years might consider shifting income recognition forward to take advantage of current rates. Advisors can collaborate with CPAs to develop timing strategies around invoicing, collections and expenses.

Phaseouts of business income deduction and AMT exemption may increase taxable estates

Two other notable provisions sunsetting in 2025 are the 20% qualified business income (QBI) deduction and the expanded alternative minimum tax (AMT) exemption amounts. While these changes have broad financial planning implications, they can also impact estate planning by potentially increasing a client’s taxable estate.

With the loss of the qualified business income (QBI) deduction, affected business owners could see a jump in their taxable income, which may push them into a higher bracket and over the estate tax exemption. Advisors should work with these clients’ CPAs to explore entity restructuring to manage income tax liability and potentially preserve estate tax exemptions.

Similarly, the AMT may ensnare many more taxpayers post-2025, as the exemption amounts will revert to their much lower pre-TCJA levels. Common AMT triggers like high state and local taxes, significant capital gains, and incentive stock option exercises could inflate a client’s taxable estate. Advisors may want to encourage clients to accelerate income and exercise ISOs while the expanded AMT exemption remains.

Flexibility is key in an uncertain future

With any planning around future tax changes, the only certainty is uncertainty. It’s impossible to predict exactly what the legislative landscape will look like in 2026 and beyond.

It’s possible that many parts of the TCJA could be extended by Congress before the 2025 sunset. However, given the current political landscape and growing national debt, many experts view this as unlikely.

Even if an extension does occur, it may not be permanent. This creates an environment of uncertainty that makes long-term planning difficult—the approach for advisors and clients should be to hope for the best but plan for the worst.

That’s why, above all, advisors should prioritize flexibility in their clients’ estate and tax planning. Rigid strategies based on current law could backfire if the rules change unexpectedly. Instead, focus on crafting nimble plans that can be easily adjusted as circumstances change.

Some key ways to build flexibility into client plans include:

Revocable trusts: Unlike irrevocable trusts, revocable living trusts can be freely amended or revoked by the grantor during their lifetime. This allows clients to modify their plans as needed without losing control of trust assets.

Disclaimers & powers of appointment: Including disclaimer provisions and powers of appointment in estate planning documents gives beneficiaries the ability to adjust inheritances based on the prevailing tax environment. This can help optimize tax outcomes without locking clients into an inflexible structure.

Regular plan reviews: Advisors should commit to meeting with clients at least annually to review estate plans and tax strategies. Regular check-ins provide opportunities to assess how changing laws and circumstances may impact clients’ plans and make proactive adjustments.

Ultimately, the key to navigating the TCJA sunset successfully is to stay informed, start planning conversations early and remain adaptable. By taking a proactive approach, advisors can strengthen client relationships and cement their value as trusted guides through an uncertain tax landscape.

When creating your estate plan, it’s important to understand the critical roles you may need to name to manage your affairs. Among these roles are conservators, guardians, trustees, executors and agents, each serving distinct functions and responsibilities.

Knowing the nuances and potential intersections of these roles will help guide your decision on whom to choose for each one.

In this article, we cover the tasks of each role, where they may overlap and how you can approach choosing someone to fullfill each one.

What is a conservator?

The court appoints a conservator to oversee the finances of an individual declared unfit to manage their own affairs, thereby protecting those incapacitated due to physical or mental disabilities.

For example, a conservator may be named if a person experiences a sudden mental breakdown, if they become severely disabled, such as paralysis, or have chronic drug use. Well-known cases include Brian Wilson of The Beach Boys or Britney Spears, who both were placed in conservatorships for mental health reasons.

The main responsibilities of a conservator include financial management, such as paying bills, managing investments and ensuring that any financial obligations of the individual are met. A conservator usually retains a lawyer to ensure compliance with court rules, which typically include keeping the court up-to-date on the person’s financial obligations and actions taken.

Most often, a conservator’s responsibilities are limited to financial oversight. But other types of conservatorships include:

General: A conservator has complete oversight over all aspects of a person’s decisions.

Limited: This type gives the conservator control over certain aspects of the person’s life. This may allow a mentally disabled adult autonomy over most aspects of their life but requiring a financial allowance and/or health treatments.

How is a conservator named?

A conservatorship usually begins with a petition being filed with the court. The person who filed the petition, like a family member or parent of an adult child, details why they want a conservatorship. They typically need medical documentation proving that the individual is unable to live independently.

During the scheduled hearing, the court evaluates the evidence and hears testimonies from various parties, including the petitioner, other family members and medical professionals.

If a court approves the petition, it will select a conservator who is willing and able to serve. The person who files the petition may suggest themselves, or they can recommend someone else, but the judge will ultimately decide who is the best person.

How long does a conservatorship last?

The length of a conservatorship depends on the situation. In emergencies, a short-term conservatorship may last about 90 days. In the case of a temporary conservatorship, the length will be determined by the court.

A permanent conservatorship lasts indefinitely. Its length will vary depending on updates from the conservator and the reasons it was established. The court can revoke a permanent conservatorship if it decides it’s no longer needed.

What is a guardian?

A guardian is the person you choose to care for your children if something happens to you. Most often, the term “guardian” refers to a child or minor. The guardian has broad oversight decisions for your child, the same you have as a parent.

A guardian can also be named for an adult. The term is sometimes used interchangeably with “conservator.” The differences are typically that guardianship refers to physical custody of the person, much like the guardian of a child, while a conservator manages their finances.

How is a guardian named?

You can name the guardian for your children in your estate plan. You can name multiple people in order of preference in case the chosen guardian is unable or unwilling to take care of your child.

It’s important to make the decision carefully. Consider whether you trust them to raise your children according to their wishes, provide for them financially (especially regarding your estate’s assets) and the quality of life they’d be able to provide.

You should always talk to the person you’re choosing to make sure they’re willing to take on the responsibility. Failing to discuss your choice may result in their refusal to serve as your children’s guardian. If this occurs and no alternate guardians are named, the court will decide. Usually, this will be the closest family member, like a grandparent, uncle or aunt, based on the court’s assessment.

An agent is the person you name in your Financial Power of Attorney (FPOA) or Advance Health Care Directive (AHCD) to make decisions on your behalf if you become incapacitated.

The term “agent” may refer to someone who can make medical or financial decisions for you, should you not have the capacity to do so.

You can provide the agent with broad or limited powers over decisions, such as overseeing only specific financial decisions or transactions. It’s usually recommended that when creating your Financial Power of Attorney and Advance Health Care Directive that you be as specific and comprehensive as possible in what decisions they can make on your behalf. Otherwise, there’s a risk that their ability to make decisions for you could be delayed or negated due to vagueness or a dispute from another party, like a family member, hospital or financial institutions.

How is a Financial Power of Attorney or healthcare agent named?

You are able to name these people in your Financial Power of Attorney and Advance Health Care Directive documents.

You can update or revoke these documents if you wish to name someone else in the future.

How does a power of attorney agent interact with a guardian or conservator?

Naming a power of attorney gives you a significant level of control over who will make decisions for you if you become incapacitated—without having to go to the courts.

The agent may even eliminate the need to name a guardian or conservator for an adult. This can simplify the process of managing decisions during incapacity.

However, if there are any disputes about the scope of the power of attorney’s role, or if they were only granted limited decision-making authority, a court may still step in to name a conservator or guardian. Still, the agent(s) you named may still be able to help guide the court’s decision during hearings.

What is a trustee?

A trustee is a person (or corporate fiduciary like an investment firm or bank) who you name to be responsible for managing the assets held by your trust.

They manage the assets that you have placed in the trust, such as cash, stock or investment accounts or your home. They must make decisions about how to protect and grow the value of those assets.

They also oversee the distribution of those assets in the trust according to the terms you have set. This may be making direct payments to beneficiaries or allocating resources for specific purposes, like school tuition.

They must also maintain accurate records of all transactions and actions they take as well as periodic reports about the performance and status of its assets. The trustee may also be responsible for filing and paying taxes for assets in the trust.

How is a trustee named?

When you create a trust, you name the person in the trust document itself. You (the grantor) can designate either individuals, like a family member, or an institution, like a bank, to serve as trustees.

If you prefer to choose an individual, you should consider a few factors, including their financial acumen, trustworthiness and willingness to take on the responsibilities. It’s important to make sure the person you choose doesn’t have any conflicts of interest. This will help maintain trust in their decision-making.

If you don’t have any family or close friends who you believe have the financial knowledge needed to manage a trust, then you can choose to have a bank or trust company act as the trustee.

In the case that the trustee is unwilling or unable to serve, the court may appoint one based on the laws of your state and needs of the trust. This is why it’s important to choose someone carefully and discuss the decision with them.

How does a trustee interact with a conservator, guardian or power of attorney agent?

There is likely to be overlap with a trustee and a conservator, guardian or an agent under a power of attorney. Since a trustee is only managing assets held in a trust, they will likely need to coordinate with any of these roles that may need to access those assets.

For example, if you die and the guardian you named in your estate plan is now caring for your children, your trustee will manage any distributions from the trust pertaining to the care of your children. How so depends on the terms of your trust.

If you specify that your children receive a set amount every year from the trust, the trustee must coordinate that distribution with the guardian. If you specify that the trust pay your child’s tuition, that must also be coordinated with their guardian.

This scenario is similar for conservators or power of attorney agents. If a person is under conservatorship, the conservator would coordinate with the trustee to manage any distributions for the benefit of the person.

Similarly, a trustee may collaborate with a power of attorney agent to ensure alignment on any actions under the terms of the trust.

What is an executor?

Your executor is the person you name who is in charge of administering your probate estate after you’re gone. This person is responsible for collecting your assets, paying your debts and distributing your probate estate to your beneficiaries.

Because property passing through a trust or beneficiary designation would typically avoid probate, such property would not typically be managed by an executor.

How is an executor named?

You can name your executor in your Last Will and Testament. If you have a trust, you are able to name your executor in your Pourover Will.

While having a trust in place typically avoids the probate process, anything left outside of the trust may go through the probate process so it’s important to still have a will in place, and have an executor named.

As with other important estate planning roles, it’s important to choose your executor carefully. It should be someone that you trust to both follow the wishes you’ve laid out as well as navigate the probate process, including the financial and legal aspects.

It’s always recommended that you talk to the person before you name them to make sure they are willing and able to serve as your executor. While they may want to consult with an estate attorney and/or financial professional during the probate process, it’s important that they understand the responsibilities.

If you don’t name someone, the person refuses or the person you named dies, the court will appoint an administrator. This typically begins with a surviving spouse or other close adult family members.It’s important to review your will periodically to make sure the person you have named is still the right choice. You are able to update your will if you wish to name a different executor because you may no longer trust the person you originally named, if they are no longer living or if you just have a change of heart.

How does an executor interact with a conservator, guardian, trustee and power of attorney agent?

While managing the probate process, the executor will likely need to coordinate with various role, including a conservator, guardian, trustee and/or power of attorney agent. For example, if you were under a conservatorship when you die, your executor will likely need to work with your conservator to administer distributions and other management aspects the conservator was involved in.

An executor would coordinate with a guardian you named for your minor children when it comes to managing their inheritance and how it’s distributed.

If you have a trustee, meaning you have a trust in place, the executor is likely overseeing the probate process for assets that were left outside of the trust which the trustee is not managing. However it’s possible they will still need to coordinate on distributions, debt collections or other aspects of your estate. If a power of attorney was used prior to your death, your executor might consult with your agent about any ongoing financial obligations or other considerations that were in place and should be considered during the probate process.

Can a conservator, guardian, trustee, executor and power of attorney agent be the same person?

Yes, the roles of a conservator, guardian, trustee, executor and agent under a power of attorney can be fulfilled by the same individual. As noted above, naming an agent in a Financial Power of Attorney and/or Advance Health Care Directive may negate the need for a court to name a conservator—or streamline the process of naming one—should the situation arise.

However, when creating your estate plan you can decide that the trustee of your trust, the guardian of your children, the executor of your will and the agents you name in your FPOA and AHCD documents are all the same person.

For example, you could decide that your sibling is whom you want to take care of your children if you die, make financial and health decisions if you become incapacitated, manage your trust and over see any probate process when you pass.

If you do arrive at that decision, make sure you understand the nuances of each role and that you trust one person to do it all, should it become necessary. While having a single person assuming all those responsibilities could simplify things, there is the risk that it could be too much for them to take on which could create issues.

Whomever you decide to name in these roles, creating an estate plan is critical to ensure that your wishes are carried out by the people you prefer and to minimize the need for the courts to make those decisions for you.

Ready to help your clients with their estate plans?

If you’ve wondered if your client needs a Credit Shelter Trust, this episode details their value in estate planning. Hosts Anne Rhodes, Thomas Kopelman and David Haughton discuss why Credit Shelter Trusts are designed for estate tax planning, specifically to preserve the estate tax exemption for spouses. They go into the different ways Credit Shelter Trusts can be structured and the potential downsides of using one. They also touch on Survivor’s Trusts and why flexibility in estate planning is so important.

If you have any experience with estate planning, you’ve heard about probate, most likely in the context of avoiding it.

But what is probate, exactly? And why is it often a “dirty” word in estate planning? In short, it’s the legal process that plays out after you die. It’s often recommended you avoid it because it can take time, it can be costly and it’s usually a public process.

That said, probate isn’t always something you need to (or can) fully avoid. But there are ways to ensure the process is, at the very least, streamlined. Typically, this is done by creating a Last Will and Testament or funding a Revocable Trust.

In this article, we break down what probate is, what you need to know and how a will and trust impacts the process.

What is probate and how does it work?

Probate is the legal process involving a court after someone dies to oversee the administration and distribution of the assets in their estate. Assuming the person has a will in place, the typical probate process includes:

Filing the deceased person’s (the “Testator”) will with the court to validate it.

The court officially appoints the executor (sometimes referred to as a “personal representative”) named in the will.

The executor takes an inventory of all assets in the estate. Some states also require a formal appraisal of all, or certain, assets.

The executor notifies any creditors and beneficiaries about the person’s passing as well as the existence of the will and the probate process.

All outstanding debts brought forward through creditor claims, such as credit card balances, are paid by the executor from the estate in addition to filing and potentially paying income and estate taxes.

The court resolves any disputes or disagreements among beneficiaries.

Finally, all remaining assets in the estate are distributed by the executor to the beneficiaries named in the will and they submit a final report to the court to close out the estate.

Voluntary administration for smaller estates

For smaller estates, many states offer an expedited process sometimes referred to as “voluntary administration.” This allows for a simplified, less formal process but still requires court oversight.

There may be fewer steps involved and it can be more of an administrative process than a legal one.

While voluntary administration can be a less complicated process, it is still technically considered probate.

How probate works without a will

The steps above are how the probate process plays out if there’s a will in place. Without a will in place, it will follow similar steps but is likely to be even more complicated and drawn out.

Dying without a will is known as intestate. If a person dies without a will, their assets are distributed according to their state’s intestacy laws, a process overseen by the court. Typically, this will follow the hierarchy of familial relationships, prioritizing spouses and children first, then parents or siblings and so on.

When someone dies intestate, the court appoints an administrator to manage the estate in place of an executor named in the will. The court may choose to appoint a surviving spouse or close family member but it is ultimately the court’s decision.

Reasons to avoid probate in estate planning

There are three main reasons you should avoid probate or at least streamline the process as best as possible: it can take a long time, it can be costly and it’s a public process.

How long does the probate process take?

Courts are notoriously slow. Probate can take months or even a year—sometimes even longer. Anyone with an interest in the estate can contest it. Even those that aren’t named in the will, but believe they should have been, may be able to contest it if they claim the will was created fraudulently or under the influence of someone else.

There is also a mandatory notice period for creditors that often lasts around six months. During this time, creditors are able to come forward and file claims against the deceased person’s estate. Assets typically cannot be distributed to beneficiaries until this process is completed.

Even if nobody contests the will and the process is as smooth as possible, it’s likely to take at least a few months before beneficiaries receive any assets.

How much does probate cost?

Probate can be an expensive process and the costs can reduce the value of the estate, ultimately leaving less to pass onto the beneficiaries.

Potential costs include attorney fees, court filing fees, executor or administrator fees and asset appraisal fees. Additionally, there could be costs associated with filing tax returns or selling property or assets, if necessary.

For smaller estates, especially, even moderate probate fees can eat into the estate’s value, seriously cutting into any inheritance designated for beneficiaries or even for charities.

Is probate a private process?

The probate process is often a public one. This is true even if you have a will because they must be filed with the court. That means that everything contained in the estate and/or the will becomes part of the public record, including who inherits what, the value of the state, debts and liabilities and even any family disputes.

Most people probably don’t want much of this information public, and doing so could create further complications. For example, making details of the estate or will public could invite people to contest its details.

Trusts, on the other hand, typically keep these details private, though there are exceptions detailed below.

How can you avoid probate?

In short, having a Revocable Trust is the most likely way you can avoid probate.

Assets passing through a will almost always need to go through probate. That’s because it’s a legal document that doesn’t actually have any legal effect until you die and then a court signs off that it’s valid.

Having a Revocable Trust, on the other hand, is like having a legal agreement with yourself to hold assets in the name of the entity. If you then transfer assets to that entity, that agreement dictates what happens to those assets when you die, not the court. Meaning, you will likely bypass probate by having a fully funded trust.

However, there are other ways to avoid probate as well. If assets pass to an individual automatically as a result of a beneficiary designation or joint ownership with rights of survivorship, these assets likely will avoid touching the probate process.

Common probate pitfalls

While having a Revocable Trust means your estate is likely to avoid probate, there are still situations where you risk entering probate with a trust.

The most common risk with a trust is that it’s not funded properly. If any assets aren’t properly transferred into the trust, those assets may go through probate.

One common example is out-of-state properties, which are often overlooked when funding a trust. If you own real estate in any other state(s) than where you legally reside, those properties may require a separate probate process. This is known as ancillary probate.

Revocable Trusts are often paired with a Pourover Will to “catch” assets not in the trust. But just like a Last Will and Testament, the Pourover Will must go through the probate process, along with any assets it “catches.”

Is it best to choose a will or trust to avoid probate?

While probate can come with some significant drawbacks—associated costs, time delays and a loss of privacy about the details of the estate—it doesn’t necessarily mean it should be avoided at all costs.

While a will is subject to probate, it still may be a valid choice for many people. It’s a simpler and more straightforward process to create one, and in some states it may be more cost-effective than a trust.

A will also allows you to name guardians, detail how assets should be distributed and name an executor that you trust to manage your estate after you pass.

A Revocable Trust, on the other hand, can cost more upfront. It also involves funding the trust with your assets, and may involve retitling certain assets like your home. If it’s set up and funded properly, however, you’re more likely to bypass the probate process.

A will likely makes sense if you have a smaller estate or aren’t concerned about aspects of probate, like delays or privacy issues. Otherwise, a trust is the best choice to avoid probate.

No matter the case, everyone needs a will. As mentioned above, if you create a trust then you’ll typically have what’s called a Pourover Will, which is a will that directs all assets to the trust in the event a probate is necessary for any assets. This type of will acts as “clean-up” in the case assets inadvertently did not get funded to the trust.

Ultimately, the decision for which type of estate planning document you want also comes down to associated costs of funding a trust at the front of the process versus paying probate costs out of your estate after you pass. Either way, having a Last Will and Testament or a Revocable Trust in place is always recommended to streamline the probate process or avoid it altogether.

Interested in how you can help your clients protect their legacies and optimize their estate plans? Schedule a demo

So you and your spouse, or partner, are creating your estate plan for the first time. Early on in the process, you’re likely to be faced with the decision of setting up a single Joint Revocable Trust or separate Individual Revocable Trusts.

Knowing which is best for you both may not be immediately obvious, and you should take the time to understand the differences between the two to come to a decision.

There are a lot of factors you should consider, including:

Your estate planning and legacy goals and wishes

Your family situation, e.g. if you have previous spouses or a blended family

If separation or divorce is a concern

If asset protection from creditors or legal issues is a concern

If you and your partner are legally married or not

The article below digs into these factors as well as the pros and cons of each type of trust to help you make an informed decision about your estate plan.

First, do you need a trust?

If you’re not sure if you should have a trust in your estate plan—let alone choose which type of trust—here are a few reasons why you should consider having one in place:

To avoid probate. Trusts help bypass the probate process, which can be lengthy and costly, so that your assets are distributed quickly and privately.

To protect and control asset distribution. Trusts provide a way to protect assets from creditors, lawsuits (like divorce), and even from mismanagement by beneficiaries by providing specific instructions for how assets are distributed to them. The grantor (the person who sets up the trust) can include further instructions for how their assets in the trust should be distributed and to whom.

Planning flexibility. Trusts can be tailored to meet a number of goals and wishes, from providing for children or those with special needs to laying out how a business you own should be dealt with after your death.

Tax efficiency. Depending on the trust and how it’s structured, you may be able to minimize estate and gift taxes, leaving more of your assets to pass onto your beneficiaries.

It should also be noted that this article is focusing on revocable trusts. As the name suggests, a revocable trust can be “revoked” or updated by the person(s) who set it up. Sometimes referred to as “Living Trusts,” they allow for more flexibility in your estate planning, especially if you expect your situation to change in the future.

An irrevocable trust, on the other hand, cannot be easily revoked or changed. However, an irrevocable trust—and there are multiple types—are often used for greater asset protection and tax strategies, as assets placed in them can be removed from your taxable estate. Though this could often result in the grantor losing control of those assets placed in the trust. Irrevocable trusts are also often used by those with more complicated and/or high-net-worth estates.

That said, revocable trusts are a great vehicle for many people due to their flexibility and ability to both help avoid probate and provide a seamless transfer of assets upon your death.

As a couple, your next decision is whether to create and maintain separate trusts or create one together. Below, we go through some factors that can help you decide what is best for you and your spouse or partner.

What is the difference between an individual trust and a joint trust?

If a couple opts for individual trusts, each person will create their own trust separately. This means both you and your significant other will maintain control over your respective trust, allowing each of you to independently manage your assets. Each person is able to determine how their assets are distributed, name their own beneficiaries, and set specific terms for how their trust is managed.

Alternatively, a joint trust is a single trust set up by both of you together. Assets are combined into one entity and managed jointly by you and your significant other. This represents a unified estate plan for your shared financial goals and intentions.

What are the pros and cons of an individual trust?

Just because you are married, or in a committed relationship, it doesn’t necessarily mean a joint trust is the right, or best, decision for you.

Individual trusts allow each spouse or partner to have control over their assets and their estate plan. Having separate trusts could make sense for couples that may differ in their approach to who should control which assets or how those assets should be distributed after their respective deaths.

You may also want separate trusts if you have concern over how your spouse or partner may handle certain assets after you pass.

Here are some factors that you should consider about an individual trust:

Strengths of an individual trust

1. Simple administration upon death

With an individual trust, asset administration becomes more straightforward upon death. It reduces confusion because the assets are already segregated between you and your deceased spouse. This helps streamline the process of transferring assets to the beneficiaries named in the deceased spouse’s trust.

2. Separate control over your estate plan

If you and your significant other prefer to have separate control over your assets, an individual trust allows for that rather than tying assets together in a single trust. This could be a benefit for those that may have previous marriages or children from a prior relationship and want to manage assets for those beneficiaries separately. It can also be a benefit in case you separate or divorce, since your estate plans are already separated and can help protect assets in any potential legal proceedings.

3. Allows for certain spousal gifting strategies

Individual trusts can simplify certain financial strategies, such as gifting assets to your spouse or significant other. For example, if one spouse needs to qualify for Medicaid, their assets can be moved out of their name and into the other spouse’s name. This allows one spouse to qualify for Medicaid benefits while still protecting the assets of the healthy spouse. It should be noted in the Medicaid example, however, that laws differ by state and you’ll want to understand the laws in your state if this may be a priority for you both when creating your estate plan.

4. Asset protection in certain situations

Individual trusts may protect assets in situations where one partner is exposed to legal or financial risks. By keeping assets separate, this could shield the other spouse from exposure to creditors or lawsuits.

5. Greater flexibility for beneficiaries

Individual trusts create more flexibility for couples that may have blended families or differ in their goals for how their assets should be distributed. Each person can structure their estate plan to suit their individual goal without needing to compromise the other person.

Weaknesses of an individual trust

1. Complexity during life

Having two separate trusts can certainly create complications for you and your partner. Especially if you want to keep the balance between both relatively equal. Doing so requires frequent monitoring and adjusting, which could be more time-consuming compared to a joint trust.

2. Higher administrative costs

Creating two separate trusts could result in higher legal and management costs. Each trust also requires its own documentation and could result in separate tax filings, which could create additional costs over time.

3. Potential for conflicts in decision-making

With each partner or spouse having full control over their own trust, this could lead to conflicts if both of you are not completely aligned on your financial and estate planning goals. This could be about which assets are put into each trust, if the trusts are equally balanced (or not), or if changes should be made to one, or both, of the trusts.

What are the pros and cons of a joint trust?

Creating separate individual trusts could require more oversight and frequent adjusting, but it could also lead to more streamlined decision making and execution upon death.

That said, a joint trust may require less management while you’re alive but it could create more complications at death or if you and your significant other were to separate.

Here are some factors to consider about a joint trust:

Strengths of a joint trust

1. Simplified and convenient asset management

Unlike needing to manage two separate trusts, you and your significant other will have all assets consolidated into a single trust. This helps reduce the paperwork and complexity of managing multiple trusts and also streamlines the process of moving assets into a single trust. If you want to make updates, it’ll be easier to do with a single trust versus separate ones.

2. Reflection of shared goals

A joint trust provides a cohesive estate plan that reflects the financial plan of both you and your spouse. It helps both partners agree on a single approach for how assets are to be distributed and aligns legacy planning.

3. Easier administration upon death

A joint trust creates a smoother transition of assets when one partner dies. With assets already consolidated and clearly designated, it creates even more protection from probate and allows for a smoother transfer process to the living spouse and/or beneficiaries.

4. Fosters clear communication

With a joint trust, both partners need to be on the same page. While that could cause some tough conversations up front, before the trust is created, it helps foster open and clear communication about what your shared goals and wishes are. It also creates transparency in handling shared finances.

Weaknesses of a joint trust

1. Complications in the event of divorce or separation

A joint trust can be problematic if you get a divorce, or decide to separate, since both of your assets are combined in a single legal entity. This can make dividing those assets time-consuming and, potentially, costly due to legal disputes. This can all be compounded if there’s a blended or complicated family situation.

2. Conflict due to differing estate planning goals

While creating a joint trust can help open up communication between you and your spouse, it can also lead to conflicts if you’re unable to resolve differences. For example, you may have a dispute about leaving assets to children from a prior marriage or which of your children should receive a certain family heirloom. Both of you must agree on the terms of the trust and it creates the possibility of opening up disagreements.

Even after a joint trust is established, you must both agree on any updates or changes you’d like to make. If one spouse wants to make an update, but the other disagrees, this can obviously create a conflict.

3. Potential lack of asset protection

Unlike two individual trusts which can help shield assets if one spouse runs into financial or legal issues, a joint trust means your pooled assets are potentially at risk in these situations.

Further factors and considerations when choosing a trust

Beyond these pros and cons for each type of trust, there are other factors that you should consider when deciding which is best for both of you.

These include:

Estate size and complexity: Larger estates or those that may involve more complex needs or distribution rules may benefit from individual trusts while a joint trust may be preferred for simpler estates.

Blended families or previous marriages: If you or your partner have previous spouses or children from a prior relationship, you may opt for individual trusts to separate control over certain assets.

For example, if you and your spouse have a joint trust and after one of you passes, a family member is upset that they are not named as a beneficiary, or are unhappy with the terms of the trust, they could try and contest it in court. If they are successful, that could throw out the entire trust for the spouse that’s still alive.

Your goals for managing your estate and finances: Some couples prefer to manage their finances jointly, while others prefer to do so separately. That doesn’t mean your estate planning needs to match but you should consider if you and your partner prefer to keep things separate or want to manage your estate together.

The state where you live: There may be nuances depending on the state where you live that could affect whether a joint or individual trust is the best choice. For example, if you live in a community property states—meaning assets acquired during marriage are jointly owned by both spouses, regardless of which person actually is named on the title or earned the income—a joint trust may make the most sense.

Currently, there are nine community property states: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin. Alaska is also a community property state but only if both spouses opt in through a community property agreement.

Furthermore, how your state deals with estate tax may impact your decision to have joint or individual trusts. An example would be in a state like New York, which has a state estate tax that’s separate from the federal estate tax. Individual trusts may make sense in this case so that each spouse’s estate is able to use their full estate tax exemption. With a joint trust, you may forfeit some of those tax advantages because assets become blended between you both.

Whether you’re legally married or not: For those that aren’t legally married, a joint trust could complicate issues—especially if you and your partner don’t or can’t file joint tax returns. If you each need to file separate, individual tax returns, you’ll need to keep track of the income generated in the trust separately.

This can lead to tax reporting and accounting complexities, particularly when it comes to dividing trust income, capital gains, or deductions because each person must accurately report their portion of the earnings. Furthermore, having a joint trust can blur the lines of ownership which could complicate the issue even more.

Should you choose individual trusts or a joint trust?

Ultimately, the decision comes down to your goals and wishes each of you have.

If you have a simple estate, have no concerns about divorce or separation, and are in agreement with how your assets should be managed while living and after death, a joint trust is likely a good choice.However, if your estate is complex, your assets are considered high- or ultra-high-net-worth, you prefer to manage assets separately from each other, or have different views on how certain assets should be distributed, creating separate individual trusts may make the most sense.

You and your partner should sit down and discuss these with each other, and understand how you each want to approach legacy planning. It’s always recommended that you also discuss these factors with your financial advisor, CPA and/or an attorney in your state to help weigh the pros and cons against the financial plan you already have.

Also remember, both types of trusts are revocable—meaning they can be undone. While doing so could be messy depending on the terms of the trust, it’s something that can be done if needed.

A critical part of estate planning is deciding how to distribute your retirement assets, such as IRAs or 401(k)s. You can name either individuals or a trust as beneficiaries of your retirement accounts. This strategy can offer certain benefits, particularly in terms of control and protection, but it also comes with potential tax implications and administrative complexities. That’s why those considering naming a trust as a beneficiary should approach the decision very carefully.

That said, the decision ultimately comes down to what your goals and priorities are. So it’s important to consider the potential benefits and disadvantages of naming a trust, and how that may affect your overall estate plan.

In this article, we explain all you need to know, including pros and cons of naming a trust for your IRA, to make the most informed decision you can.

What are the benefits of naming a trust naming a trust vs. individual as an IRA beneficiary?

There are a number of reasons why you may want to choose a trust as your IRA beneficiary. But, the main reasons are usually about exercising control over how the assets are distributed and to provide potential protection from creditors.

Here are a few reasons why it may make sense for you:

1.Control over the distribution of assets

If you have beneficiaries who are minors, have special needs, or lack financial responsibility, naming a trust provides more control over how retirement account assets are distributed. You can specify conditions in the trust, such as age milestones for access, specific uses for the funds, or annual withdrawal limits.

2.Protection from creditors or divorce

A trust can act as a barrier from potential creditors, lawsuits, or divorce proceedings. Naming a trust as the beneficiary can help prevent the funds being accessed in those types of situations.

3. Multi-generational wealth preservation

A trust can be used to help preserve assets from a retirement account for future generations, such as children or grandchildren, by staggering the distribution over many years.

4. Managing complex family dynamics

If you have a complex family dynamic, such as a previous spouse, children from previous relationships, or estranged family members, naming a trust as the beneficiary can ensure assets are distributed according to your wishes if there are any family disputes, rather than being distributed according to default state laws.

5. Centralizing asset management

Naming a trust can be part of a strategy to consolidate multiple types of assets under a single entity, making it easier for a trustee to distribute according to your wishes, as well as handle any other administrative tasks or investments. This may be particularly relevant for those with larger estates or managing multiple beneficiaries.

Even if any of these reasons are a priority for you, you should still understand the potential disadvantages of naming a trust before following through, if only to make sure you fully understand the decision and you’re not hit with any surprises.

What are the disadvantages of choosing a trust as your retirement account beneficiary?

The primary drawback of naming a trust as a beneficiary of an IRA or 401(k) mainly has to do with taxes. Trusts don’t typically enjoy the same tax advantages of an individual. For instance, it’s much easier for a trust to hit the top tax bracket—37%—than it is for an individual.

Here are some common disadvantages of naming a trust as a beneficiary of your retirement account:

1. Trusts have higher tax rates

Because trusts have more “compressed” tax brackets, they reach higher tax rates at much lower income levels than individuals—hitting the highest rate at just $15,200 of income. This risks reducing the amount passed onto the people named in your trust as beneficiaries.

It’s important to note, however, that there are ways to get around having the trust pay the taxes (more on this below).

2. Less flexibility

Once you name a trust as the beneficiary, changing it later could prove complicated—though not completely undoable. But, remember, trusts are legal entities that include special instructions and may have limited ability to adapt to beneficiary needs, law changes, or just your overall wishes, especially if it’s an Irrevocable Trust.

3. Risk of mismanagement by the trustee

A trust requires you naming a trustee, someone to oversee its management, including the distribution of funds and other administrative tasks. While a trust includes special instructions, some may not be “codified” and may be left as recommendations the trustee should follow but isn’t required to follow.

While the trustee should be someone you trust to manage everything, there is always the possibility that someone that’s inexperienced or has conflicted interests may not do so effectively.

4. It can introduce numerous complications

Naming a trust as a beneficiary, unlike a person, can complicate how funds are withdrawn and taxed. These rules vary by the type of trust, making it difficult for an inexperienced trustee to manage without help from professionals like attorneys, financial advisors, or tax experts..

Again, these are just a few potential drawbacks. It’s also important to dig into a bit more about taxes, withdrawal rules, and the impact of 2019’s SECURE Act.

How the SECURE Act of 2019 impacts naming a trust as a beneficiary

2019’s SECURE Act made major changes to inherited retirement accounts, with the IRS issuing its final regulations in 2024. These had some major implications on how One of the biggest updates is that many who inherit a retirement account would be subject to the 10-Year Rule and required minimum distributions (RMDs). This rule also applies to trusts in most situations. Here’s what you need to know about navigating these changes.

Loss of the “stretch” rule

Previously, most trusts could stretch retirement account distributions over a beneficiary’s life expectancy. However, the SECURE Act now limits this period to 10 years, creating potential tax challenges.

Trustees face a decision: either spread withdrawals over the 10-year period or take smaller required minimum distributions (RMDs) annually and withdraw the bulk in the 10th year. Both strategies risk higher tax brackets because the IRA or 401(k) must be emptied by the end of the 10 year period.

In some cases, a 5-year rule may apply instead of the 10-year rule, which could present even greater tax disadvantages, depending on the type of trust.

When the 5-year withdrawal rule applies

The 5-year rule may apply in the following circumstances:

1. Non-designated beneficiaries. If you name a non-designated beneficiary, such as a charity or estate when the account owner dies before their RMD age, and the beneficiary does not qualify for the 10-year rule.

2. If the trust does not qualify as a “see-through” trust. A trust must meet certain conditions to be considered “see-through.” If not, the 5-year rule may still apply.

How to avoid the 5-year withdrawal rule

To avoid the 5-year withdrawal rule, the trust being named as the beneficiary of an IRA or retirement account must be considered a “see-through” trust. If it is considered a “see-through” trust, then the 10-year rule will apply, per the SECURE Act (again, the “stretch” rule would have applied prior to the SECURE Act).To be considered a “see-through” trust, it must meet four requirements:

1. The trust must be valid under state law.

2. The trust is irrevocable or becomes irrevocable at the death of the grantor (the person who set up the trust).

3. The beneficiaries of the trust are identifiable.

4. The trustee has provided the custodian of the retirement account with the trust document by October 31 of the year that follows the grantor’s death.

Once the trust has been established as the “see-through” trust, it must then be determined what the payout period is for the IRA based on the underlying beneficiaries. This depends on whether the trust is a conduit trust or an accumulation trust.

Here are the differences between the two:

Conduit Trust: This type of trust requires that all IRA distributions are paid directly to the trust beneficiaries. The IRS looks at the life expectancy of the beneficiary to determine RMDs, but under the SECURE Act, these distributions must still follow the 10-year rule in most cases.

Accumulation Trust: This type of trust allows IRA distributions to be retained in the trust for further management and control. However, the IRS considers the age of the oldest trust beneficiary to determine the applicable RMD period, which could also be within the 10-year window.

Why do these withdrawal rules matter?

The major disadvantage of the new 10-year rule is that it can have a significant impact on the trust’s taxable income, thereby risking reaching a higher tax bracket. If the trust is subject to the 5-year rule, it’s an even bigger disadvantage.

However, they don’t apply to spouses named as beneficiaries. Another major advantage of naming a spouse is that they are able to roll over any inherited IRAs or 401(k)s into an account in their own name.

Can a person pay the taxes instead of the trust?

Trusts reach the highest marginal tax rate on income much faster than individuals. However, if the trustee distributes income to the trust’s beneficiaries, those individuals can report the income on their personal tax returns, potentially at a lower tax rate.

This approach is often possible with a Grantor Trust. In this context, however, the trust would not be considered a Grantor Trust since the grantor would be deceased. For other types of trusts, avoiding trust tax rates requires specific provisions in the trust agreement. The trustee must have the authority to distribute the trust’s income directly to the beneficiaries and issue a Schedule K-1 (Form 1041).

Trustees might choose this strategy when the beneficiaries’ personal tax brackets are lower than the trust’s tax brackets, optimizing tax efficiency. This decision must be weighed carefully, considering the beneficiaries’ financial circumstances and any potential conflicts.

In such cases, the trustee can issue a Schedule K-1 (Form 1041) to the beneficiaries, allowing them to report the income on their personal tax returns.

These details must be correctly set up in the trust before it is named as a beneficiary to avoid unintended tax consequences.

So while it’s possible to avoid the tougher trust tax rates, doing so still involves nuances and potential complications. That’s not to say that it should deter you from this strategy but it’s important to understand the nuances and that it may be best to consult with an estate attorney when setting up your trust if naming it as an IRA beneficiary is your intention.

So should you name a trust as a beneficiary to your IRA or 401(k) or not?

There isn’t a right or wrong answer. As detailed above, there are valid reasons to name a trust as the beneficiary of your retirement account. And there are reasons you may not want to.

In most circumstances, it may be best to name a spouse as the primary beneficiary because they are not subject to the SECURE Act’s 10-year withdrawal rule or the mandatory RMDs. And they are able to roll over any inherited accounts into an account under their own name—meaning it’s not counted as taxable income.

Ultimately, the decision usually comes down to control versus tax and cost efficiency. If having control over how the retirement assets are distributed is a major concern and you care less about maximizing the amount, then naming a trust may make the most sense. However, if you want to maximize the amount that passes onto your beneficiaries and don’t mind there being less control over how those beneficiaries receive and/or use the funds, naming them directly likely makes the most sense.

Either way, it’s a crucial decision and one that should be made carefully. It’s always recommended that you work with your financial advisor or a tax professional to approach the decision that makes the most sense for you and your situation.

So you’ve created, or updated, your estate planning documents. Congratulations! You’re at the final stretch but there’s one more important step you may need to take: Your documents need to be signed and notarized.

Getting your documents notarized serves a few purposes but the most important one is that without getting notarized, they may not be considered legally valid. That could open your estate up to potential probate proceedings or other court challenges.

We recommend following this process:

Print your documents, or request them to be shipped to you.

Take them to be signed in front of a notary (additional witnesses may be needed).

Scan your notarized documents and upload them into your wealth.com Vault for security and accessibility.

Below we’ll detail more about the process, our recommendations and answers to common questions.

What does it mean to get estate planning documents notarized?

Getting a document notarized is when a notary public certifies the authenticity of signatures on a document. Typically, the process involves:

Identity verification. The notary verifies that the person signing is who they claim to be. They typically ask for identification in the form of a driver’s license or passport.

Witnessing the signature. A notary also needs to witness first-hand the person signing the documents willingly and not under coercion. Some states may require additional witnesses.

Notarial seal and signature. After the notary confirms the above, they include their signature and their official or stamp confirming that the document is now legally valid and credible.

Why is a notary needed?

The primary reason for getting documents notarized is for your protection. First, to ensure that documents aren’t fraudulently signed in your name. For example, somebody signing a will in your name that you did not actually sign—like something out of a movie plot.

Second, to ensure that the documents are recognized by the legal system if, and when, they need to be executed. The last thing you want to happen with your estate plan is for there to be unnecessary legal action because the validity of the documents you signed is questioned. By getting documents notarized, when they need to be executed there is confirmation that you have willingly signed them and they can be legally executed because you followed your state’s regulations for getting them notarized.

How can I get my documents notarized?

Requirements for how to get documents notarized vary by state. Each state has its own laws and regulations governing how notarization works. Differences between states may include identification requirements you can use or if you need additional witnesses as well as training requirements for notaries themselves.

If you need to notarize your documents, you can actually order a mobile notary directly within Wealth.com. We offer a nationwide network across all 50 states of trust-certified notaries who can meet you at a preferred date, time, and location. Your advisor doesn’t need to coordinate this appointment, since our mobile notary preferred provider, Sign Here Ink, manages all orders and scheduling. Our mobile notaries also bring printed copies of your documents to the appointment, so there’s no need to print them yourselves. Once the appointment concludes, the notary will leave the original documents with you to keep and scan a digital version for your advisor same-day to download. It’s that simple! If you’re a Wealth.com user, you can learn more about how to request a mobile notary your Help Center or by asking our AI assistant.

You can also find a notary at a local UPS or FedEx location. Banks also often have notaries on staff, although you may need to be a customer to use them. You can also search online for local notaries near your home. The benefit of going to a UPS or FedEx location is that you can print your documents there (if you don’t have a printer at home), get them notarized on site and then scan the signed documents and have them emailed to you so you can upload them to your secure Vault.

When you print your wealth.com documents, details for getting them notarized in your state will be included.

Are online notary services also available?

Online notary services are legal to use in some states but you should use caution if you choose to use one. That’s because while they can legally operate in some states, there still may be legal requirements that could conflict or create confusion with the use of an online notary.

For example, New Jersey allows remote ink-signed notarization but doesn’t recognize remote online notarization—the difference being the need for a wet signature. However, that ability to get it remotely can easily cause confusion.

Furthermore, some online notary services may not accurately follow state-specific instructions if they operate in multiple states, opening you up to potential issues in the future.

Legislation in a number of states is likely to continue to be updated, with the hope that remote online notarization becomes a simpler process. We are actively monitoring legislation across the country and will notify you—via instructions when it’s time to sign your documents—if remote online notarization is allowed in your state.

Until then, we do recommend an in-person notary as the best way to ensure that you minimize any potential legal issues if, and when, your documents are executed in the future.

Can I get my documents notarized in another state?

It’s recommended that you follow your state regulations and also discuss with your notary. Technically, a notary can legally notarize documents from any state as long as the notarial act occurs in the state in which they were commissioned because notaries are typically only verifying the signer’s identity and not the document itself.

However, best practice would be to confirm with the notary that they don’t believe this would be an issue. We also recommend extreme caution in this instance that the document is being notarized according to the instructions of the state they were produced in.

What if someone named in my estate plan is also a notary?

It’s not usually recommended that any interested party notarize or witness any estate planning documents.

Certain states will strike the nomination as executor or gift to a beneficiary if a witness is the individual named as either. Even without a specific statutory prohibition in a given state, it opens the door for all kinds of litigation arguments around undue influence and capacity in execution

In the latest episode of The Practical Planner, Anne Rhodes and Thomas Kopelman sit down with Chris Nason, a partner at McDermott Will & Emery LLP and a Trust and Estate Planning teacher at Stanford University. Chris provides a deep dive into The Tax Cut and Jobs Act of 2017, sharing insights on how advisors can craft effective estate planning and tax strategies before its benefits sunset at the end of 2025.

Don’t miss out on this valuable discussion to help you stay ahead in advising your clients.

Justin Castelli, Founder of RLS Wealth, joins hosts Anne Rhodes and Thomas Kopelman to talk about how his approach to financial planning has shifted to focus on life planning by placing a focus on his clients’ life goals and values at the center rather than focusing on the numbers first. By helping clients figure out what their authentic life looks like and how to achieve it, he believes it brings more clarity to the estate planning process. Check out this episode to hear how he helps clients figure out what’s most important in their lives and how that helps them plan for what happens when they pass.

Estate planning can be difficult due to tough conversations you may need to have and make. This can be exacerbated by certain cultural and generational expectations and taboos.

Anna N’jie-Konte, CFP®, President and Director of Financial Planning at Re-Envision Wealth, joins this episode to share how financial advisors can help their clients approach these conversations and why having them now can be beneficial for all their family and loved ones.