Financial Power of Attorney Explained

So much of estate planning is thinking through how you want things handled after you die, before you start actually making a documented plan. The idea of a financial power of attorney (FPoA) flips that a bit, because it’s about appointing someone to handle your affairs in case you become incapacitated and can’t make your own decisions. The process seems complex, but we’ll simplify it so you can make sense of the basics you need to know to include this important element in your estate plan.

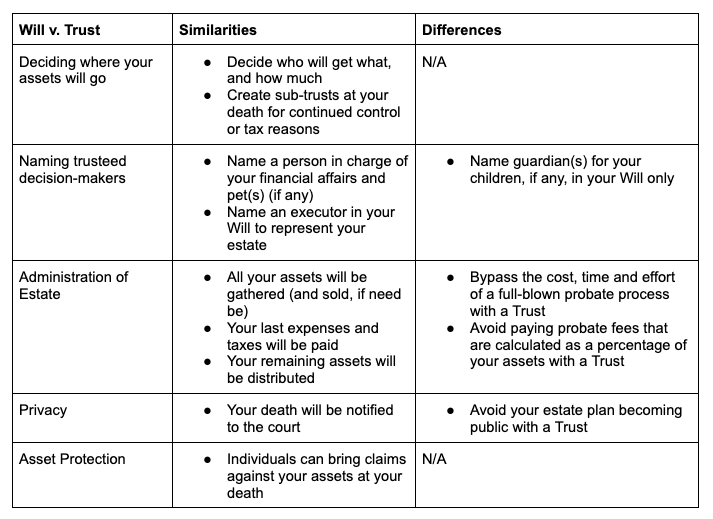

What Role Does a FPoA Play in Estate Planning?

In a nutshell, a financial power of attorney is a document in which you appoint a trusted person to act on your behalf to make financial decisions. In establishing a FPoA, you hand over the legal reins to another person to conduct financial transactions, sign documents, or make other legal decisions as if they were you. This might happen for only a limited period of time (during a serious illness or after an accident, for example), or it can take effect immediately upon signing and last up to your end of life. Once your FPoA is completed, your trusted person, the agent, sometimes called an attorney-in-fact or fiduciary, can be responsible for managing your financial affairs. You will need to use a second document, called an Advance Health Care Directive (sometimes known as health care proxy or health care power of attorney), to designate who should handle all of your medical decisions. There are several types of FPoA, so consider the specific needs of your estate before selecting one.

Durable Power of Attorney

The type of FPoA most commonly used in estate planning is a durable power of attorney. “Durable” indicates that your agent has your permission to act on your behalf even though you are incapacitated or disabled. In other words, the FPoA is effective until you either revoke the document or have passed away.

You can spell out your agent’s powers, responsibilities and restrictions in the FPoA. The powers vary from state to state but usually include the ability to:

- Sell or manage property and real estate

- Sign legal documents and checks

- Manage personal and business-related financial accounts

- Pay medical bills (but not make healthcare decisions)

- File taxes and settle claims on your behalf

Hire professional assistance, such as a lawyer or advisor

Non-Durable Financial Power of Attorney

When an FPoA is not “durable,” your agent’s powers end when you become incapacitated or disabled. In other words, you want to supervise your agent’s use of the FPoA powers. This can be a good option for transactions that are not driven by estate planning needs. For example, you might grant your advisor a non-durable FPoA to conduct time-sensitive trades on your behalf.

In addition, you may be comfortable allowing your agent to change your estate plan or the rights of your beneficiaries; because these are such sensitive powers, in most states, you must affirmatively grant each estate planning power.

Why Include a Durable Power of Attorney in Your Estate Plan?

A complete estate plan should provide not only for death, but incapacity and unavailability. Putting a FPoA in place allows someone to continue managing your financial affairs if you cannot sign important documents yourself in case of emergency, a routine surgery, or even travel abroad.

Keep in mind that to complete your FPoA, it must be signed in accordance with your specific state’s requirements, which might mean signing before a notary public or witness(es).

The wealth.com platform makes it straightforward to get your Financial Power of Attorney drafted and securely stored in our Vault, and provides state-specific guidance on how to fill out and sign your FPoA.

Get this guide to Financial Power of Attorney as a printable PDF

Download PDF