TL/DR: Estate planning isn’t as complex as it may seem and you don’t need a legal degree to create one. In short, estate planning is simply recording your wishes for what happens if you’re unable to manage your own affairs. This quick and comprehensive overview will give you a working understanding of the estate planning basics.

________________________________________________________________

No one likes to think about death, especially their own. But think about this: What will happen to your stuff—money, family heirlooms, even a pet—if something happens to you? If you haven’t created a document that tells your loved ones who should get what, and who should sign off on those decisions and do all the paperwork, your loved ones will have to decide for (and potentially argue among) themselves. You can provide for your family’s needs, ensure your wishes are honored, and save your loved ones a lot of anguish during an already stressful time by creating an estate plan.

Although estate planning is essential for ensuring your money and property are distributed in exactly the way you want, only one-third of adults in the U.S. have a Will. That overall number has fallen steadily over the past five years, but the COVID-19 pandemic did inspire those ages 18 to 34 to write a Will—63% more people in that age group created a Will in 2021 than in 2020.

So why don’t more people do it? The five main reasons are:

- I just haven’t gotten around to it.

- I don’t have enough money saved.

- I don’t know how to begin.

- I don’t know anything about it.

- I don’t own anything valuable.

Unfortunately, these misconceptions are preventing people from putting even a basic plan in place. People perceive estate planning to be complicated, scary, or simply not relevant to them. The reality is, you don’t have to be a millionaire or own multiple homes to benefit from an estate plan.

You need an estate plan if:

- You worry that your pet(s) could be given to a shelter

- You want to make a final gift to a grandchild, niece, or nephew, or a friend or charity at your death

- You have specific wishes about your health care and end-of-life care

- You feel strongly about who should manage your affairs if you were unable to do so yourself

- You really want your children to end up with your assets, if there is anything left after your spouse passes away

- Some of your family members don’t get along and might disagree about who gets what or who should manage your affairs

- You do not want a certain family member to receive your assets, to make health care decisions for you, or to manage your affairs

- You own a significant amount of cryptocurrency

Do any of these sound like you? Because most everyone can benefit from the peace of mind an estate plan brings, we want to demystify the process so everyone—yes, even those without a law degree—can see that it’s simpler and more accessible than they think. And, hopefully, the information in this guide will equip you with enough information to quit putting off this important task.

Getting Started: Estate Planning Documents

At its most basic level, estate planning is making preparations for when you’re no longer able to make decisions for yourself. It requires creating and signing a few legal documents; but more importantly, it requires thoughtful decisions so that the money and possessions you have earned and accumulated can be passed down to your family or whomever you choose.

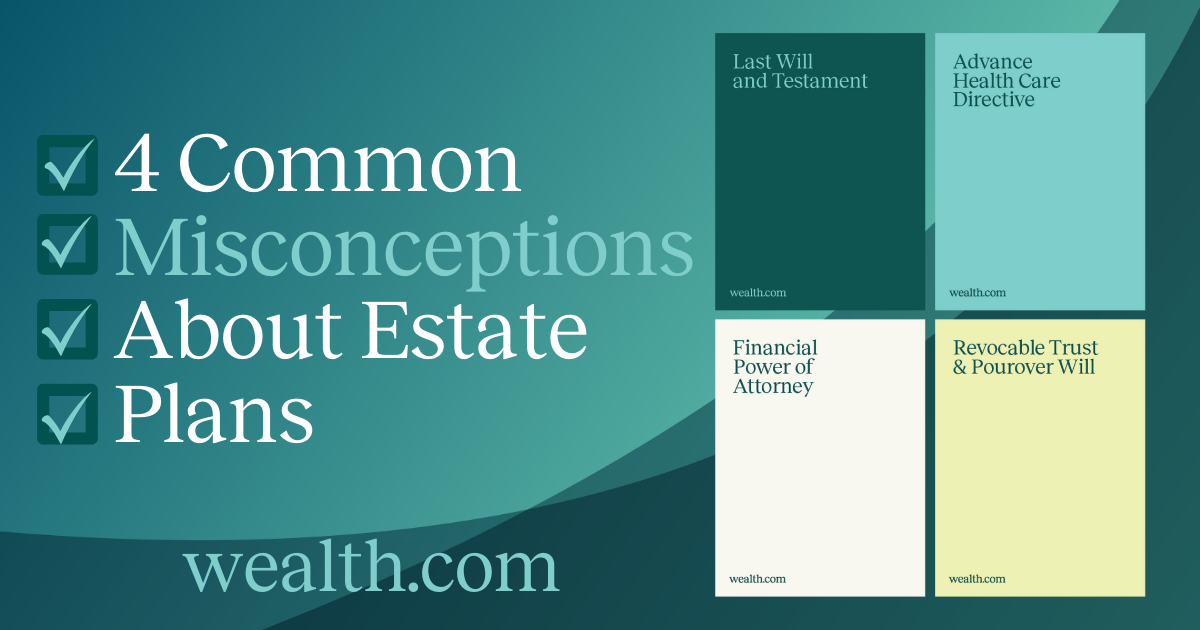

Let’s talk about what you’ll put in place as part of a basic estate plan. The legal documents are:

- Last Will and testament: This document, which becomes active after you die, expresses your wishes for how to divide up your property and possessions and names the people you prefer to manage your financial affairs (the “executor”) and take care for your children who are minors or have special needs (the “guardian”). A revocable Trust can offer some advantages over a Will (more on Trusts vs. Wills here). However, you can only designate an executor or a guardian through a Will, not a Trust. For this reason, you still need a short Will (called a “pourover Will”), even if the centerpiece of your estate plan is a Trust.

- Financial power of attorney: Think of this document as a permission slip that gives the person you name (the “agent”) the ability to conduct financial transactions, sign documents, and make other legal decisions as if they were you. In most states, you can choose if your agent has this permission immediately after you sign or only once you are incapacitated. This document terminates at your death.

- Advance health care directive: This document empowers the person you name to make decisions about your medical treatment, symptom management, and end-of-life care. Depending on your home state, this document may go by a variety of different names, including a health care power of attorney or proxy. The document usually includes or is paired with a living will, which are your written instructions for health care providers about the type of life-prolonging medical care you want to receive if you are unable to make decisions for yourself.

- Trust: A Trust is created by a contract or agreement and acts like a bucket of “stuff.” The Trust agreement is the set of rules that the creator of the Trust puts in place for the trustee who oversees the Trust. The rules include what powers the trustee has over the Trust, to whom and under what circumstances the trustee can give assets out of the Trust. After you create a Trust, you can transfer your assets into the Trust right away, before you die. There are many types of Trusts that accomplish different goals. If you create a Trust as the centerpiece of your estate plan instead of a Will (more on Trusts vs. Wills here), you will set up a type of Trust called a “revocable Trust” or “living Trust.” You will be the trustee of your revocable Trust in the beginning. You can also designate the person who will step in for you as trustee so that when you are unable to manage your own affairs eventually, that successor trustee can distribute your stuff according to your instructions. Unlike a Will, a Trust is active the day it is created, which means that your successor trustee can also help you manage the stuff inside of your Trust in case you are incapacitated.

There are two types of Trusts.

- Revocable or living Trusts can be altered at any time by the creator of the Trust (you). These Trusts are often used as a substitute for a Will in estate planning.

- Irrevocable Trusts are difficult and expensive to alter once created. They can be used to achieve many types of goals, including minimizing taxes protecting assets from creditors, naming an adult to manage property for children before they reach a certain age, and ensuring that assets stay within the same family. In your Will or your revocable Trust, you can instruct your executor or trustee to create an irrevocable Trust to take advantage of the benefits of irrevocable Trusts.

Why Do I Need an Estate Plan?

No one needs an estate plan. That is, unless you want to avoid confusion, chaos, hurt feelings, family drama, and delayed distribution due to probate. So, maybe you do need one?

An estate plan lets you give the gift of clarity to your loved ones—and does all the legal heavy lifting so they don’t have to. When you spell out your wishes in the legal documents listed above, there’s less second-guessing about your intentions for how your stuff should be distributed.

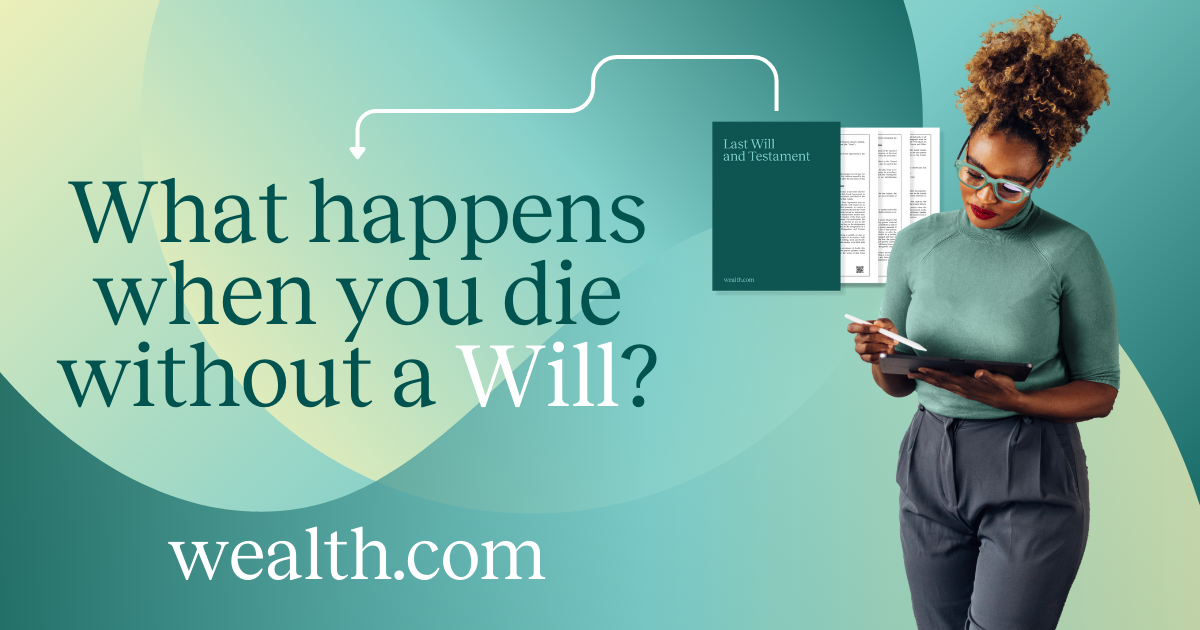

The opposite is true if you die without a Will or Trust in place. Legally, you are dying intestate, and your home state’s succession laws will determine how your assets will be distributed and to whom. These succession laws differ from state to state, but were likely drafted a long time ago, based on the most common wishes of a typical, American nuclear family, and likely do not reflect the complexities of your family and cultural heritage.

By not creating an estate plan, you are just letting the state legislature from decades ago take a guess as to what your wishes are. This is especially true if you’re single and don’t have dependents.

You may own assets that will not pass through your estate, either because of the title on the asset or because you designated a beneficiary. For example, jointly owned property–real estate, a car, or bank account–will automatically pass to the survivor, or you may have designated a beneficiary for a life insurance policy or retirement account. However, it is still important to have a Will or a Trust for several reasons. Certain assets must pass through your estate (for example, personal objects or cryptocurrency), so the only way to direct where they go at your death is through a legal document. Having no assets in your estate will make it difficult to pay for your last expenses, including funeral costs, legal fees, and any taxes.

Who’s Involved in an Estate Plan?

Now that we’ve looked at the important reasons why to have an estate plan, it’s time to turn to the who in an estate plan.

The most important person is you, the creator of the Will (testator) or Trust (called grantor, settlor, or trustor–not to be confused with the trustee!). By taking the time for careful consideration and creating various legal documents, you are establishing clear expectations for how you want your money and property to be handled upon your death.

The other essential players involved in estate planning include:

Beneficiaries: These are family members, loved ones, or charitable organizations—anyone who receives an asset of yours in your Will or Trust. Assets can include cash, real estate, or that piano you inherited from your grandparents.

Heirs: If you die without an estate plan (or all the beneficiaries you listed in your estate plan have passed away or otherwise do not qualify to receive your assets), the people who will receive your assets are known as your heirs. Your heirs are determined under default succession laws. They are not necessarily the people you would have named as your beneficiaries.

Executor: If you create a Will, you will name an executor (sometimes called an administrator or personal representative) to manage your affairs after you die. This person will collect your property, pay any debts and taxes, and distribute the remaining property according to the terms of your Will. This often takes a bit of legwork, including contacting banks, investment and insurance companies, and appraisers.

Trustee: When the centerpiece of your estate plan is a Trust rather than a Will, this person manages your affairs just like an executor would. Because the roles are so similar, generally the same person is named in the role of successor trustee and executor. Moreover, if you put assets into your Trust during life, the trustee can manage them during your incapacity, instead of relying on a financial power of attorney.

Agent or attorney-in-fact: Not to be confused with an actual lawyer, this is the person you named in your financial or health care power of attorney to act or make decisions on your behalf.

Guardian: If you have children who are minors or have special needs, this is the person you name to care for the wellbeing in case both you and the other parent are unable to care for those children.

If you’re wondering whether a lawyer is also part of this list, it depends. Most people can set up and manage their estate plan on their own using online tools, like Wealth, which are backed by extensive legal expertise.

When you put together the what, why, and who behind estate planning, you can see it really boils down to thinking about and documenting your final wishes, then appointing someone you trust to be in charge of executing those wishes after you die. It’s a simple, thoughtful act that protects your family and your legacy.

We hope these explanations have shown that estate planning is important but not impossible. Like death itself, it’s not something people talk about much, which has led to a myth that it’s too complicated for the average person to tackle. The reality is, estate planning takes time and consideration, but it’s time well spent to safeguard your loved ones’ wellbeing.