Gifting plays a crucial role in wealth transfer planning, allowing individuals to support loved ones, fund education, and optimize their estate plans. As a financial advisor, understanding and discussing gifting strategies with your clients is essential, particularly with the potential tax law changes set to take effect at the end of 2025.

The Tax Cuts and Jobs Act (TCJA) significantly increased the lifetime gift and estate tax exemption, but these provisions are set to sunset after 2025, reverting to pre-2018 levels. While the Trump Administration is pushing to make these tax cuts permanent, high-net-worth clients who haven’t yet taken advantage of the elevated exemptions may still want to consider accelerating their gifting plans.

Here’s what advisors need to know to guide their clients through the complexities of gifting and help them optimize their wealth transfer plans.

Understanding the basics of gifting rules and exemptions

To effectively guide clients, advisors must grasp the basics of gifting rules and exemptions:

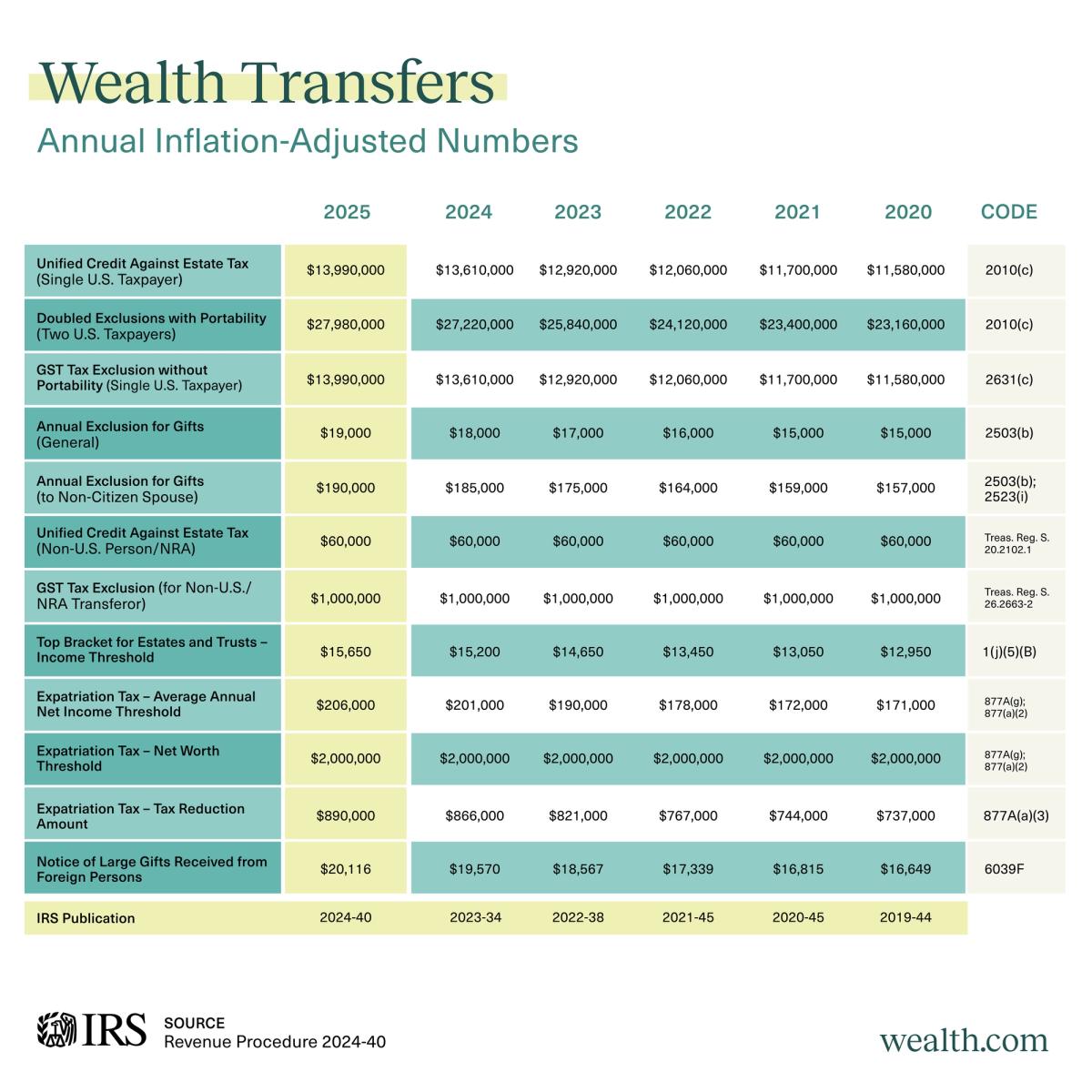

- Annual exclusion: In 2025, individuals can gift up to $19,000 per recipient without triggering gift tax reporting. Married couples have the ability to combine their annual exclusions to gift up to $38,000 per recipient. This amount is indexed for inflation and may increase in future years.

- Lifetime gift tax exemption: The current lifetime gift tax exemption is $13.99 million per individual in 2025 but is set to revert to an estimated $7 million (adjusted for inflation) after 2025 if the Tax Cuts and Jobs Act sunsets.

- Gift tax reporting: Gifts exceeding the annual exclusion may require filing Form 709, even if no gift tax is ultimately owed due to the lifetime exemption.

- Unlimited gifting exceptions: Direct payments for educational expenses (tuition only) and medical expenses are exempt from gift tax limits. This means that paying a grandchild’s college tuition or a parent’s hospital bill should not typically count towards the annual exclusion or lifetime exemption.

- Estate tax interplay: Taxable gifts made during life reduce the available estate tax exemption at death. This creates an interconnected planning dynamic, where lifetime gifts and bequests at death must be strategically balanced.

Tailoring gifting approaches to client wealth goals

Effective gifting strategies often vary based on a client’s wealth level and goals. Here’s a high-level breakdown:

Mass affluent clients ($5M or less)

For clients with more modest estates, consider these simpler gifting strategies:

- Direct family gifts: Annual exclusion gifts of cash, property, or other assets to children, grandchildren, or other relatives can help support their financial needs while incrementally reducing the taxable estate.

- Education funding: Contributing to 529 plans for children or grandchildren’s education qualify for the annual exclusion, and some states offer additional tax deductions or credits. Plus, the assets grow tax-free if used for qualified education expenses.

- First-time homebuyer assistance: Helping family members with down payments on a first home is a popular gifting strategy. These gifts can be structured as annual exclusion gifts, or larger amounts can be reported as taxable gifts using the lifetime exemption.

- Charitable giving: Modest charitable gifts, whether direct donations or through donor-advised funds, can provide income tax deductions and reduce the taxable estate.

High-net-worth clients (Over $5M)

Wealthier clients, especially those with estates exceeding the current lifetime exemption amount, may benefit from more advanced gifting structures:

- Irrevocable trust strategies: Grantor Retained Annuity Trusts (GRATs) can transfer appreciating assets to beneficiaries with minimal gift tax impact. Irrevocable Life Insurance Trusts (ILITs) remove life insurance proceeds from the taxable estate. Charitable Remainder Trusts (CRTs) provide an income stream to the grantor while benefiting charity and reducing the taxable estate.

- Family limited partnerships (FLPs): FLPs pool family assets under a central entity and allow for discounted gifting of partnership interests.

- Dynasty trusts: These long-term trusts are designed to minimize estate and generation-skipping transfer taxes over multiple generations.

- Charitable giving: Private foundations and charitable lead trusts allow for more specific philanthropic impact while offering estate and gift tax benefits.

Navigating the tax landscape of gifting

Gifting strategies can have large tax implications that advisors must help clients navigate:

- Basis considerations: Gifted assets generally retain the donor’s cost basis (known as “carryover basis”), which can lead to larger capital gains taxes for recipients if the assets are later sold. Inherited assets that have appreciated typically receive a “stepped-up basis” to fair market value at the owner’s death, potentially reducing capital gains for heirs.

- Generation-skipping transfer (GST) Tax: Gifts to grandchildren or later generations (known as “skip persons”) may trigger an additional 40% GST tax without proper allocation of the GST exemption (which currently mirrors the gift and estate tax exemptions).

- State-specific issues: Some states also impose their own estate or inheritance taxes with exemptions far below the federal amount. States may have separate gift taxes.

- Income tax implications: Certain gifting strategies, such as transferring appreciated assets or creating grantor trusts, can impact the donor’s income tax situation. For example, income generated by assets in a grantor trust is taxed to the grantor, not the trust itself.

- Timing considerations: Advisors should help clients time gifts strategically. For example, gifting appreciating assets early shifts future growth out of the taxable estate. With the potential impending reduction of the gift and estate tax exemptions in 2026, planning to utilize the higher exemptions before they sunset could yield significant tax savings.

Debunking gifting myths: What clients need to know

Navigating gifting strategies can be complicated, and clients often have misconceptions that advisors must address:

- Clients may not realize that some gifts need to be reported even though they are under the lifetime exemption amount. It is important that clients are aware of their tax reporting obligations, even if it will not actually result in a tax liability being due.

- Some clients confuse gift tax and estate tax rules, not understanding that taxable gifts during life also reduce the available estate tax exemption at death. Others may think that all gifts are inherently taxable or that only cash gifts need to be reported.

- Clients often don’t realize that indirect gifts, like paying a family member’s expenses or forgiving a loan, can count as reportable gifts. Helping with a down payment, covering medical bills (if paid directly to the provider), or even adding a joint owner to a bank account all have potential gift tax implications that need to be properly tracked and reported.

- The difference between “carryover basis” for gifts and “stepped-up basis” for inheritances is a frequent point of confusion. Clients may not know how gifting an appreciated asset during life can lead to higher capital gains taxes for the recipient compared to leaving that same asset as a bequest at death.

To help clients visualize potential gifting scenarios and their impact, consider leveraging Wealth.com’s Scenario Builder. While advisors cannot provide legal advice, tools like this can help inform and guide client conversations.

Conclusion

Gifting is a powerful wealth transfer strategy that requires careful planning. By understanding the fundamentals, optimizing for tax implications, and addressing common misconceptions, advisors can help clients navigate the complexities of gifting.

Remember, the advisor’s role is to educate, guide, and facilitate these conversations, not to provide legal advice. Encourage clients to consult with estate planning attorneys and tax professionals to implement their specific strategies.

As tax laws continue to evolve, advisors who engage clients in gifting discussions will differentiate themselves and provide immense value. Your clients will appreciate your initiative in helping them navigate this complex — but essential — aspect of their financial lives.